You've probably done this already. You spot a tidy apartment in Sydney or a character house near Byron Bay. The photos are sharp, the agent says the rent is strong, and the numbers look clean at first glance. Then the important question hits: is the advertised return achievable, or are you buying into someone else's optimistic spreadsheet?

That's where proper rental market analysis earns its keep. Not the lightweight version based on a few live listings, but the kind of due diligence that tests rent, tenant demand, leasing risk, expenses, and affordability pressure before you commit. In high-stakes markets, small errors get expensive fast. A rent estimate that's slightly too high can turn into weeks of vacancy, heavier incentives, and a purchase that never performs the way it looked on day one.

Key Steps for a Comprehensive Rental Market Analysis

- Beyond the Listing Price What a True Analysis Uncovers

- First Principles Defining Your Investment Objectives

- How to Gather Actionable Local Market Data

- Calculating Yields and Modelling Cash Flow

- Stress-Testing Your Analysis for Hidden Risks

- Analysis in Action Sydney vs Byron Bay Case Studies

- From Analysis to Action Your Path to a Smarter Investment

Beyond the Listing Price What a True Analysis Uncovers

A glossy listing tells you what the seller wants you to believe. A real rental market analysis tells you what a tenant will pay, how long they'll stay, and what it costs you if the estimate is wrong.

Take a common scenario. An investor sees a two-bedroom property with a renovated kitchen, polished floors, and a claimed “strong yield.” On paper it looks easy. Then you inspect the finer points. The second bedroom barely fits a bed, parking is absent, the pet policy is restrictive, and three newer complexes nearby are competing for the same tenant pool. Suddenly the “market rent” in the sales pitch starts to look like the top edge of the range, not the likely outcome.

That's the gap amateurs miss. They treat rent as a fixed number. Practitioners treat it as a range with conditions attached.

Practical rule: If the asking rent only works when everything goes right, it isn't your rent. It's a best-case scenario.

In Sydney, that often means checking whether convenience really offsets compromises like no parking, road noise, awkward floorplans, or heavy strata competition. In Byron Bay, it means asking a different set of questions. Is the property suited to stable long-term tenants, or is the local market shaped by short-term letting pressures, seasonality, and tighter local constraints than the listing lets on?

A proper assessment also protects you on the buy side. If your rent estimate comes in below the sales campaign narrative, your valuation of the asset changes with it. That's one reason many investors use a Sydney buyer's agency process that focuses on securing the right property without overpaying. The rent line drives the holding costs, the yield, and often the price you should be willing to pay.

First Principles Defining Your Investment Objectives

Most weak rental market analysis starts too late. People jump straight into suburbs, agent quotes, and rental estimates before they've decided what the property needs to do for them.

Start with the outcome, not the suburb

If you want stronger cash flow, you'll tolerate a different asset than someone chasing long-term capital growth. If you're rentvesting, you may accept a tighter yield in a market with better scarcity, stronger owner-occupier appeal, or better future resale depth. If your priority is simplicity, you'll avoid properties with operational friction even when the top-line rent looks attractive.

Write down the investment brief in plain language before you open another portal tab. The useful questions are practical:

- Income focus: Do you need the property to hold itself comfortably, or can you support shortfalls while waiting for growth?

- Growth focus: Are you buying in a market where land value, location scarcity, and resale demand matter more than day-one yield?

- Lifestyle overlap: Might you use the property yourself later, and if so, does that distort your analysis?

- Risk tolerance: Can you cope with rent volatility, stricter regulations, or longer vacancy if the market softens?

These answers change what “good” looks like. A compact apartment in an established Sydney pocket can suit a growth-led strategy even if the yield starts out tight. A different investor might reject it immediately because the holding costs don't fit their cash flow threshold.

Use objectives to filter noise

This is also where macro data becomes useful instead of distracting. Zillow reported that annual rent growth slowed to 2.1% in December 2025, down from 2.2% the month before, while the typical asking rent fell 0.2% to $1,901. At the same time, 39.5% of rentals on Zillow offered concessions, and the median household needed to spend 26.5% of income on a new rental. Zillow said that represented the most affordable conditions for renters in more than four years, with affordability improved by 0.3 percentage points from the prior year, showing that rent alone doesn't tell the full affordability story because wages and incentives matter too, as detailed in Zillow's December 2025 rent report.

The lesson for Australian investors is straightforward. Don't confuse rent movement with investment quality. A suburb can show resilient asking rents while tenant affordability is tightening underneath. Another can look softer on headline rent but remain more stable because tenants have more capacity to absorb the cost.

Your objective decides which signals matter. Without that filter, you'll chase properties that look good in a listing and underperform in your actual portfolio.

How to Gather Actionable Local Market Data

Most investors gather rental data the lazy way. They check current listings on Domain or realestate.com.au, average a few asking rents, and call it research. That's how you overestimate rent.

Build the right comp set

A disciplined rental market analysis starts with a 5–10 property comp set matched on size, location, bedroom and bathroom count, condition, and amenities. It also needs validation from both active listings and recently leased properties, because asking rents alone can mislead. Parking, furnishing quality, pet policy, and nearby amenities can materially change achievable rent and leasing speed, as explained in Mashvisor's guide to rental market analysis.

That sounds simple. It isn't. In Sydney, one street can trade differently from the next because of school catchments, traffic, rail proximity, or building quality. In Byron Bay, a house with better outdoor space, easier parking, or a less compromised layout can pull ahead quickly because tenant expectations are specific and supply is uneven.

When building your comp set, separate properties into three buckets:

- Closest matches: Same property type, similar condition, same tenant profile.

- Useful edge comps: Slightly better or slightly inferior properties that show the realistic range.

- False comps to reject: Different building quality, compromised location, or features that change the tenant pool.

Check the market beneath the listing portals

Listings tell you what owners hope to get. Leased results, days on market, and vacancy data tell you what tenants accepted.

Use the portals first, but don't stop there. Look at suburb-level vacancy trends through SQM Research, read local leasing commentary from property managers, and inspect ABS Census data for the tenant base you're targeting. A pocket heavy with transient renters behaves differently from one supported by longer-term professional households or established local families.

For Byron Bay and nearby coastal markets, I also want to know what isn't obvious in the listing data:

- Regulatory pressure: Short-term letting rules can change the effective rental strategy.

- Supply surprises: New stock, secondary dwellings, and informal competition can shift the leasing environment quickly.

- Tenant profile shifts: Holiday demand and lifestyle migration can create noise that doesn't equal stable long-term tenancy.

If you want on-the-ground help in that kind of market, Byron Bay buyer's agency support for off-market opportunities, due diligence and negotiation is one way to compare desktop assumptions against what's happening at suburb and street level.

Here's a quick visual summary before you build your shortlist:

Translate local detail into a rent decision

Good analysts don't copy the highest comp. They place the subject property within the range.

A renovated two-bed unit with no parking might sit below the best recent lease even if the kitchen is sharper. A Byron Bay house with strong privacy but awkward maintenance needs might rent well, but it may also narrow the tenant pool. The answer isn't one number. It's a pricing strategy with a likely rent, a stretch rent, and a line you won't cross because vacancy gets too expensive.

The wrong rent doesn't just reduce income. It changes who enquires, how long the property sits, and how much leverage you lose once the first campaign misses.

Calculating Yields and Modelling Cash Flow

The fastest way to fool yourself is to stop at gross yield. Gross yield is useful for triage. It is not enough to buy on.

Gross yield is a screening tool, not a decision tool

Start with the simple calculation. Annual rent divided by purchase price gives you gross yield. That helps you compare opportunities quickly, especially when you're sorting through very different stock.

After that, the work gets real. Investor-grade underwriting combines rent estimates with occupancy, time-to-lease, seasonality, and return benchmarks such as cap rate and cash-on-cash return. One cited benchmark is to target markets above 5% cap rate and individual properties above 8% cash-on-cash return, with the warning that pricing above market creates avoidable vacancy, as outlined in this rental pricing and underwriting guide.

That matters because two properties with similar gross yield can perform very differently once costs hit.

Model the cash flow that actually lands in your account

For Australian investors, the core expense lines usually include strata, council rates, water, insurance, property management, maintenance, and leasing costs. If it's a house, maintenance assumptions matter more. If it's an apartment, strata can be the deal-breaker. A building with lifts, concierge services, or deferred works can destroy what looked like a neat return.

Use a simple model with conservative rent and realistic downtime. Then test the result before tax and after key ownership costs. If you want to sharpen that side of the model, it also helps to understand legitimate ways to reduce your taxable rental income so your after-tax position isn't based on guesswork.

Here's a plain example structure you can adapt.

| Item | Amount (AUD) |

|---|---|

| Purchase price | [enter amount] |

| Expected weekly rent | [enter amount] |

| Annual gross rent | [enter amount] |

| Strata | [enter amount] |

| Council rates | [enter amount] |

| Water | [enter amount] |

| Insurance | [enter amount] |

| Property management | [enter amount] |

| Maintenance allowance | [enter amount] |

| Vacancy allowance | [enter amount] |

| Net operating income | [enter amount] |

| Interest cost | [enter amount] |

| Pre-tax cash flow | [enter amount] |

The table matters less than the discipline behind it. Every line should be defensible. If the rent is based on one optimistic comp, or the maintenance line is artificially thin, the model isn't conservative enough.

A lot of buyers also need to decide whether they are prioritising yield now or better long-term growth drivers. That's where a framework like rental yield versus capital growth in an Australian buying strategy can help keep the assessment tied to the original brief rather than the emotion of the deal.

Stress-Testing Your Analysis for Hidden Risks

The first version of a property model almost always looks cleaner than the lived reality. That's why the stress test matters more than the base case.

Test the rent, then test the tenant base

Start with rent risk. Ask what happens if the lease-up takes longer than expected or if the property needs to be priced below your initial estimate to secure a stronger tenant. Then test operating costs. Insurance can move. Repairs don't arrive on your schedule. A body corporate issue can turn a comfortable holding position into a tight one.

After that, test the market itself. A critical but often overlooked risk is whether a market is rent-stretched relative to incomes. A public New Orleans rental study found the market was “heavily dependent on subsidy” because of the gap between rents and resident incomes, which is a useful warning that headline rent growth can mask a fragile tenant base, as noted in the Greater New Orleans Housing Alliance rental study.

That principle travels well. In expensive Australian markets, the question isn't just whether tenants want to live there. It's whether enough tenants can comfortably sustain the rent you're underwriting.

Build downside cases before you buy

I like to run three versions of the same property.

- Base case: Achievable rent, ordinary downtime, expected annual costs.

- Soft market case: Lower rent, longer leasing period, more incentives required.

- Nasty case: Lower rent, vacancy at the wrong time, plus a meaningful repair item.

You don't need heroic complexity. You need honesty. If the property only works in the best-case model, you're buying risk and calling it upside.

A second hidden risk is supply timing. In fast-changing rental markets, today's comps can go stale quickly if a pipeline of new stock, concessions, or shadow inventory starts to hit. Industry data cited by IBISWorld says U.S. apartment rental revenue grew at a 3.3% CAGR from 2021 to 2026 and is projected to reach $305.7 billion by 2026, with growth concentrated in Sun Belt and Texas markets where supply and demand are shifting quickly, according to IBISWorld's apartment rental industry outlook. The broader lesson is clear. If supply changes faster than your comp set, your rent estimate can age badly within a quarter.

Don't stress-test because you're pessimistic. Stress-test because purchase decisions get made in the present, but performance happens in the future.

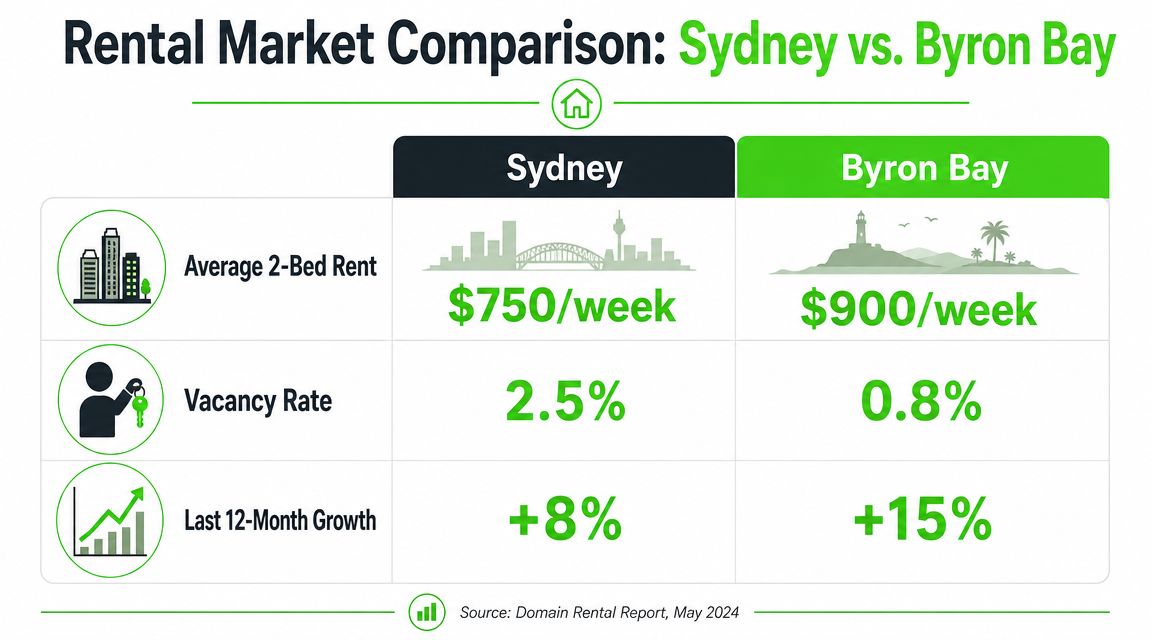

Analysis in Action Sydney vs Byron Bay Case Studies

The framework stays the same in both markets. The weight you place on each factor doesn't.

Sydney rewards discipline on asset selection

In Sydney, I'm usually less interested in the agent's rent guidance than in the property's leasing resilience. Can a good tenant see themselves living there for years, or is the asset relying on shiny presentation to hide compromises?

For an inner-city apartment, the check list is practical. Walkability matters. Rail access matters. Floorplan efficiency matters. Parking may matter a lot more than the selling agent admits. In some pockets, the difference between one secure car space and none is the difference between broad demand and a much thinner tenant pool.

Sydney also punishes lazy buying on building quality. If a unit has expensive strata, poor natural light, or obvious defects risk, a tight gross yield becomes even tighter when real ownership costs land. That doesn't mean Sydney is a bad investment market. It means the case usually rests on scarcity, location strength, and long-term appeal rather than easy day-one cash flow.

Byron Bay needs a regulation and seasonality lens

Byron Bay is different. A property there can look outstanding on headline rent and still carry more operating and policy risk than many buyers appreciate.

You need to ask whether the investment case relies on long-term rental demand, short-term letting demand, or a hybrid assumption that may not hold. Local restrictions, council settings, neighbour sensitivity, and management intensity all matter. So does seasonality. A property that performs well in a peak-demand window may not tell you much about stable annualised performance if your strategy depends on a more complex rental approach.

If you're assessing a property that may have short-term rental relevance, it helps to understand the operational side as well as the market side. These accounting tips for Sydney short term rentals are useful because they force you to think about record-keeping, expense structure, and the admin burden that often gets ignored in acquisition modelling.

What changes between the two markets

Investors often make expensive category errors when they apply the same lens to both places.

A side-by-side approach makes the differences obvious:

| Factor | Sydney | Byron Bay |

|---|---|---|

| Primary demand check | Stable tenant depth, transport, employment access | Lifestyle demand, regulation, seasonality, local supply quirks |

| Common investor mistake | Overpaying for cosmetic renovation while ignoring strata and floorplan issues | Underestimating operational complexity and policy risk |

| Rent assessment style | Tight comp matching by building, street, and amenity set | Broader context around tenant type, usage assumptions, and restrictions |

| Best use of due diligence | Screening for durable demand and avoiding expensive buildings | Testing whether the income story is robust outside ideal conditions |

One broad market point is still worth keeping in view. Rental markets have normalised since the post-pandemic surge. Baselane reported that 85% of landlords raised rents in 2024, but growth returned to a more typical 2% to 4% annual range after the extreme 15% to 20% yearly increases seen in 2021 to 2022. Baselane also found 78% of landlords planned to raise rents in 2025 by a weighted average of 6.21%, while Zillow's observed national market rate increased 3.4% to $1,964.80 over the same period, according to Baselane's rental market trends summary. For investors, that means underwriting should lean on normalised expectations, not boom-era rent jumps.

That point matters in both Sydney and Byron Bay. If your deal only works because you assume outsized rent growth continues, the analysis is too hopeful. In these markets, discipline beats optimism.

From Analysis to Action Your Path to a Smarter Investment

A buyer sees a clean listing in Sydney or Byron Bay, plugs in the agent's rent estimate, and decides the deal looks fine. That is how investors end up owning properties that look good on inspection day and disappoint for years after settlement.

Good rental market analysis turns broad market commentary into a buy or pass decision on one specific asset. It removes the stories sellers tell, replaces them with tested assumptions, and forces every number to earn its place in the deal. That matters most in expensive markets, where a small mistake on rent, vacancy, strata, insurance, or compliance can wipe out the margin you thought you had.

The process is straightforward, but it isn't casual. Start with the role the property needs to play in the portfolio. Then check whether the local tenant pool, competing stock, and ownership costs support that role. If they do not, the answer is no, even if the suburb itself looks strong on paper.

In Sydney, the winning decisions are often the ones investors do not make. Passing on poor layouts, high-fee buildings, compromised locations, or apartments with weak owner-occupier appeal protects more capital than chasing an optimistic rental figure. In Byron Bay, the work is less about headline demand and more about whether the income holds up under normal conditions, with realistic occupancy, stricter rules, and higher operating friction.

We Are Buyers Agents provides suburb analysis, property shortlisting, and inspection support aligned to an investment brief across Sydney and Byron Bay.

If you're close to buying, get an independent read on the suburb fit, rental potential, and property-level risks before you commit. Speak with the team at We Are Buyers Agents. They help investors and home buyers make decisions based on evidence, not sales talk.

Written with Outrank tool