You've got a mortgage approval, a decent cash buffer, and a banker telling you an offset account is a smart move. That might be true. It might also be an expensive extra that sounds clever but doesn't match how you manage money.

For Australian buyers, this decision matters more than it first appears. An offset loan can help reduce interest while keeping cash available for emergencies, renovations, tax bills, vacancies, or the next deposit. But the value isn't automatic. It depends on your savings habits, your loan structure, your tax position, and whether you're buying as an owner-occupier or investor.

A lot of borrowers understand the headline. Put cash in offset, pay less interest. Fewer understand the strategic part. When does an offset clearly beat a redraw? When does it protect future tax deductibility? When are you better off taking a cheaper basic loan and keeping your cash elsewhere?

If you want a broader market view beyond Australia, EHF Mortgages' offset mortgage guide is a useful companion read because it shows how the same core structure is explained in another established offset market.

Navigating Your Guide to Offset Loans

- An Introduction to the Offset Loan

- How an Offset Loan Actually Works

- Offset Account vs Redraw Facility The Critical Difference

- The Real Costs and Benefits of an Offset Loan

- Strategic Use for Investors and Homeowners

- Decision Time Is an Offset Loan Right for You

An Introduction to the Offset Loan

An offset loan is a home loan linked to a deposit account where the balance in that account reduces the amount of the loan that the lender uses to calculate interest. The key point is that the money in the offset remains your money. It hasn't been paid off the loan. It's still available to use.

That distinction is why offset loans appeal to buyers who want flexibility. If you're buying a home in Sydney, Byron Bay, or anywhere else in Australia and you know you'll keep cash on hand, an offset can turn that idle cash into a working part of your loan strategy. Salary, savings, rent received, or business cash can all sit in the linked account and reduce interest while they're there.

For owner-occupiers, the appeal is usually straightforward. You lower interest and keep an emergency buffer. For investors, the conversation gets more technical. The account structure can affect future borrowing decisions, cash flow management, and tax outcomes in ways many borrowers only discover after settlement.

Practical rule: An offset is most useful when you hold meaningful cash balances and want those funds to stay accessible.

Banks tend to sell the feature. Astute buyers need to assess the behaviour it rewards. If your account balance is usually thin, or you clear out savings as fast as they arrive, the offset may not earn its keep. If you regularly hold surplus cash, it can become one of the more flexible tools attached to a mortgage.

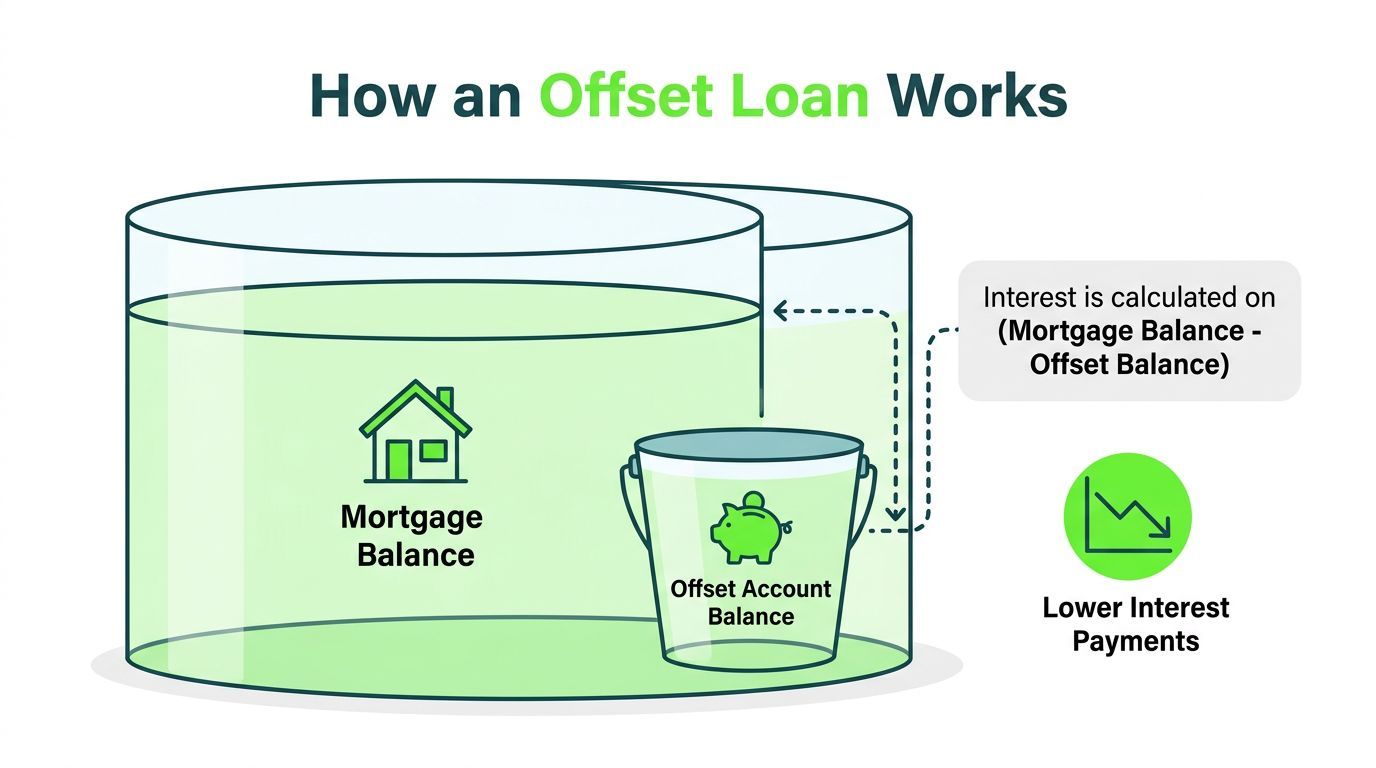

How an Offset Loan Actually Works

A clear example usually lands this faster than a definition.

The core mechanic

Say you settle on a $900,000 home in Melbourne with a $720,000 loan, and you keep $80,000 in the linked offset account for your renovation buffer and emergency funds. The lender still records your home loan as $720,000. Interest is only calculated on $640,000 while that $80,000 remains in the offset.

That is the whole mechanism. The cash stays in a separate account under your control, but the bank uses it to reduce the balance on which interest is charged.

That distinction matters in practice. If the hot water system fails, the body corporate issues a special levy, or an investor spots another buying opportunity and needs quick access to cash, the money is still available. You have not paid it into the loan. You have parked it beside the loan.

Why daily calculation matters

Most lenders calculate home loan interest daily and charge it monthly. That means the offset works best when money arrives early and stays in the account as long as possible, as noted earlier in the article.

This is why borrowers who use an offset well usually run their cash flow through it. Salary goes in. Bills come out later. For investors, rent can land there too. Business owners often use the same approach with trading cash, BAS money, or funds set aside for tax.

Small habits change the result over time:

- Salary timing matters: money sitting in the offset for even part of the month reduces the daily interest calculation.

- Irregular income helps: bonuses, commissions, rent, and contract payments can all improve the outcome while they stay in the account.

- Short-term cash reserves still work: funds set aside for renovations, rates, insurance, or tax can reduce interest until you need them.

A borrower who leaves $40,000 in a standard savings account and a borrower who leaves the same $40,000 in an offset have the same cash on hand. The second borrower usually comes out ahead if their home loan rate is higher than what that cash would have earned after tax in a savings account.

At this point, the strategy starts to matter.

For an owner-occupier, the benefit is usually straightforward. Keep surplus cash in the offset, reduce non-deductible home loan interest, and keep access to your money. In a high-rate environment, that can be a strong use of spare cash.

For an investor, the logic can be even more important, but for a different reason. If you expect the property might become an investment later, or you want to preserve deductibility on borrowed funds, holding cash in offset rather than paying down the loan can protect flexibility. Banks promote the interest saving. They rarely spend much time on how account structure can affect future tax outcomes.

There is a trap here too. An offset only earns its keep if cash stays in it. If the account balance is usually low, and the loan package charges a higher rate or annual fee for the feature, the maths can turn against you quickly.

Offset Account vs Redraw Facility The Critical Difference

A common mistake starts here. A borrower pays extra into the loan for a few years, then redraws that money for a car, school fees, or a deposit on another property. The loan still looks tidy in internet banking, but the tax position may no longer be tidy at all.

That is the difference.

An offset account keeps your cash in a separate account linked to the loan. A redraw facility gives you access to extra repayments already pushed into the loan itself. Both can reduce interest. The practical consequences are very different once you need that money back.

For owner-occupiers, redraw can be fine if the plan is simple and stays simple. Put extra money in, reduce interest, leave it there. The trouble starts when life changes. If you later redraw for private spending, you have created a new borrowing for a private purpose. If that home later becomes an investment, part of the loan may no longer be deductible in the way many borrowers expect.

For investors, or buyers who may turn their home into an investment later, this point matters more than the bank brochure suggests. Cash held in offset has not changed the underlying loan purpose. Cash paid into the loan and then redrawn can. Once a loan gets mixed between private and investment use, the record-keeping gets harder and the tax outcome can get worse.

That is why many experienced investors park surplus cash in offset rather than using redraw as a piggy bank.

Interest still falls in both cases. The difference is structure, access, and future tax treatment. If you want a broader view of how rates shape these decisions, this guide to interest rates and property investing in Australia is worth reading alongside your loan comparison.

Offset Account vs Redraw Facility at a Glance

| Feature | Offset Account | Redraw Facility |

|---|---|---|

| Where the money sits | In a separate linked account in your name | Inside the loan as extra repayments |

| Access to funds | Usually works like transaction account access, subject to lender rules | Access depends on lender redraw rules, limits, and processing |

| Effect on interest | The offset balance reduces the loan amount used to calculate interest | Extra repayments reduce the loan balance directly |

| Best use case | Borrowers who want flexibility and may need the cash later | Borrowers happy to commit surplus cash to debt reduction |

| Investor tax position | Usually cleaner because the original borrowing purpose stays intact | Can create mixed-purpose debt if funds are redrawn for private use |

| Discipline required | You need to keep cash in the account for the feature to pay off | You need to avoid casual redraws that create a mess later |

The trap with redraw is not product design. It is behaviour. People treat available redraw like savings, but it is borrowed money coming back out of the loan. That distinction matters most when the property's use changes or when redrawn funds are used across personal and investment expenses.

I see this often with first-home buyers who later keep the original home as a rental. They made extra repayments for years, then redrew part of the balance for renovations on a new home or general personal spending. The result is a split-purpose loan that their accountant now has to trace line by line. Avoiding that mess early is usually easier than fixing it later.

A practical rule works well:

- Use offset when you want full access to cash, may convert the property to an investment later, or want cleaner tax separation.

- Use redraw when you are confident the extra repayments should stay in the loan and you do not need that money for other purposes.

- Be careful with redraw if you are an investor, may become one, or tend to reuse available funds without tight records.

For borrowers focused on debt reduction, redraw can still have a place. Some households like the friction. Money inside the loan is harder to spend, and that can help. If your goal is pure repayment discipline, that may suit you better than a fully accessible offset. For strategies that prioritise flexibility while still cutting interest, this blueprint for paying mortgages early gives a useful framework.

The short version is simple. Offset is usually cleaner. Redraw can be cheaper. The right choice depends on how likely you are to need the cash again, and whether tax deductibility may matter later.

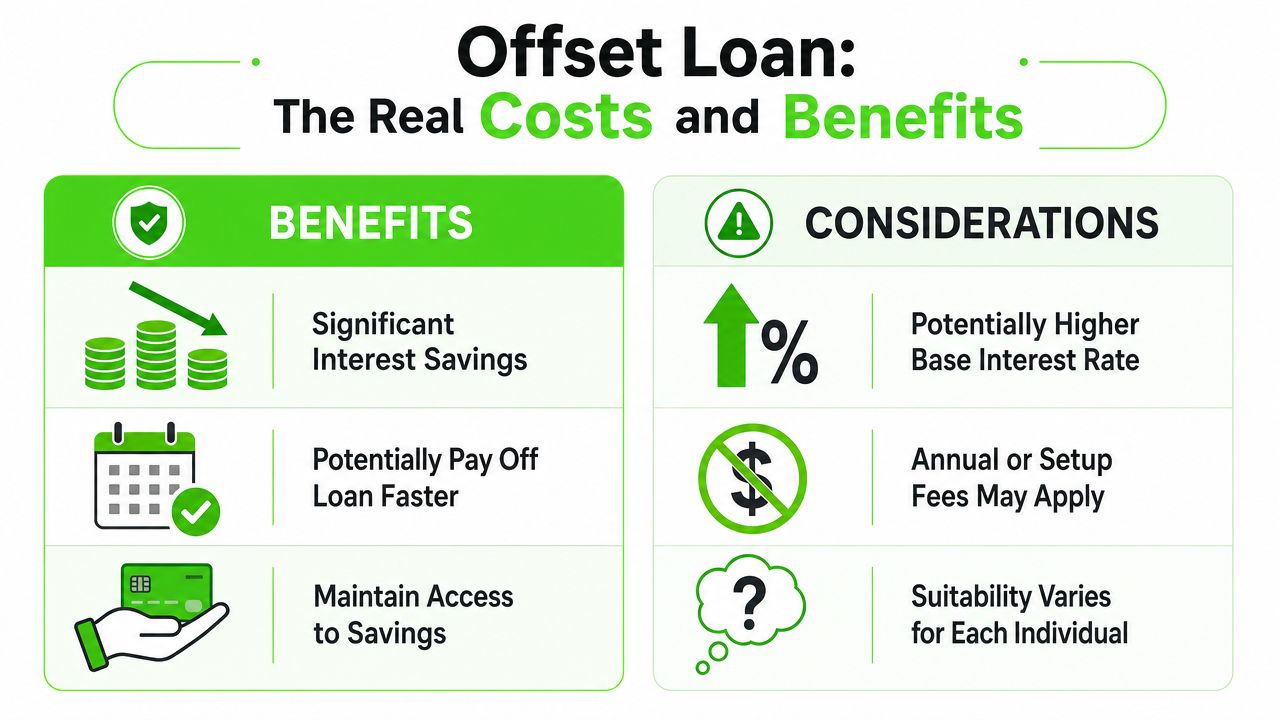

The Real Costs and Benefits of an Offset Loan

The bank's pitch is easy to like. Reduce interest. Keep access to cash. Potentially pay the loan down faster. All true. But there's a second half to the story. Some offset loans come with a higher rate, an annual package fee, or both. If you don't keep enough money in the account, the feature may cost more than it saves.

When the maths works

The central trade-off is clear in CommBank's explanation of offset accounts: the actual benefit depends on whether the mortgage rate you save is greater than the return that same cash could have earned elsewhere, plus any fees or rate premium attached to the offset feature, as outlined in CommBank's guide to what an offset account is.

That means the right question isn't “Does offset save interest?” It does. The better question is “Does this offset loan beat my alternatives after costs?”

A practical break-even approach looks like this:

- Start with the extra cost: compare the offset loan against the cheapest suitable non-offset alternative.

- Estimate your usual balance: not your best month, your normal month.

- Check the alternative use of cash: savings account, term deposit, business use, or investment opportunity.

- Factor in access: liquidity has value, especially if the cash is a genuine buffer.

If you're serious about debt reduction generally, this blueprint for paying mortgages early is a useful companion piece because it helps frame offset as one tactic within a broader repayment strategy, not a magic switch.

A related issue for buyers comparing loans is the broader rate environment. If you're weighing product features against headline cost, it helps to understand how lending settings affect strategy. This overview of Australian interest rates and investing considerations adds that context.

When an offset becomes a trap

An offset is a poor fit when the borrower likes the idea more than the routine required to make it effective.

Common warning signs include:

- Low average balances: You open the account but keep very little in it most of the time.

- Frequent cash leakage: Salary goes in, then lifestyle spending drains the account almost immediately.

- Feature-chasing: You pick the loan for the offset label without checking if the overall package is competitive.

- Wrong opportunity cost: Your cash could be doing a better job elsewhere, and you've ignored that comparison.

A good offset loan is a tool. A bad offset loan is a fee attached to a habit you don't have.

For disciplined savers, the feature can be excellent. For borrowers who don't hold cash, it often turns into a premium product with little real payoff.

Strategic Use for Investors and Homeowners

The most useful way to look at an offset isn't as a loan add-on. It's a cash management system attached to debt. That's why the strategy differs depending on whether you live in the property or hold it as an investment.

For owner-occupiers

For a homeowner, the goal is usually simple. Reduce non-deductible interest without losing access to emergency funds.

The cleanest setup is often to direct income into the offset, keep day-to-day spending controlled, and let the account operate as the household's financial buffer. That can work well for salaried borrowers, but it's especially effective for people with irregular income, such as self-employed buyers, consultants, and anyone with bonus-heavy remuneration.

What works in practice:

- Use the offset as your main transaction hub: salary in, bills out, surplus left sitting there.

- Keep your emergency reserve in the offset: not in a separate low-interest account doing nothing strategically.

- Store short-term project cash there: renovation funds, school fees, or expected annual expenses can all reduce interest while waiting to be used.

The mistake I see is fragmentation. Buyers leave money across several accounts because it feels organised, but it weakens the offset effect and usually adds no real advantage.

For investors

For investors, the offset can be less about speed and more about structure. Preserving flexibility matters. So does keeping the loan position clean if you plan to buy again, convert a home into an investment, or avoid mixing borrowed and personal funds.

In terms of strategy, offsets often beat redraw. If you hold surplus cash in an offset rather than paying it directly into the loan, you reduce interest while keeping the original loan balance intact. That can matter later if the property becomes part of a broader portfolio plan.

Investors also need to think carefully about tax treatment. The details depend on personal circumstances and professional advice, but the broad principle is that loan purpose matters. If you redraw for private use, or mix purposes carelessly, you may complicate deductibility. A general background read like this Guide to landlord tax liability can help frame why mortgage structure and tax outcomes are often more connected than borrowers assume.

If you're building or reshaping a portfolio, this guide with broader advice for property investors is also worth reading because offset strategy rarely sits in isolation from asset selection and financing structure.

Investors usually regret messy loan structures far more than they regret being slightly conservative with cash.

A practical investor use case is straightforward. You hold cash for repairs, vacancies, land tax, or the next deposit. Rather than pay that money permanently into the loan, you park it in offset. You still reduce interest, but you don't sacrifice liquidity or reshape the loan balance in a way that may limit future options.

That's the point banks often underplay. An offset isn't just about saving interest. It's about preserving choices.

Decision Time Is an Offset Loan Right for You

Most buyers don't need a more complex explanation. They need an honest filter.

An offset loan is usually a strong fit if you keep a solid cash buffer, want immediate access to that money, and are disciplined enough to make the account part of your everyday banking. It's also attractive if your income is uneven or you're an investor who cares about preserving flexibility and avoiding loan contamination.

It's probably the wrong fit if you rarely hold savings, choose loans mainly on features rather than total cost, or prefer a simpler structure that forces extra repayments into debt reduction. In that case, paying for an offset can become dead weight.

Use this checklist as a practical test.

- Savings habit: Do you consistently keep meaningful cash in reserve?

- Account discipline: Will income flow into the offset and stay there as long as possible?

- Loan comparison: Have you compared the offset option with a simpler non-offset loan on total cost, not marketing?

- Future plans: Could this property later become an investment, or could you need the cash for another purchase?

- Strategy fit: Does this structure suit your behaviour, not just your intentions?

If you're buying your first investment, this first investment property checklist for Australia is a sensible next read because offset decisions often sit alongside bigger questions about borrowing capacity, buffers, and acquisition timing.

The borrowers who get real value from offsets tend to know exactly why they have one. Everyone else is often paying for optionality they never use.

If you want help assessing the right loan structure around your next purchase, especially where offset strategy, cash buffers, and long-term portfolio planning all intersect, the team at We Are Buyers Agents can help you think through the property side of the decision before you commit.