You're probably doing what most first home buyers do at the start. Saving listings late at night, comparing suburbs you didn't even know a year ago, and trying to work out whether the home you want is merely ambitious or completely out of reach.

That mix of excitement and mental overload is normal. Buying your first place in Australia is emotional because it isn't just a transaction. It's the point where lifestyle, lending rules, government policy, and timing all collide. One wrong assumption early can cost you months. One smart move early can put you in a far stronger position than buyers who look more “ready” on paper.

The good news is you're not trying to enter the market alone. In the December quarter of 2025, first home buyer owner-occupied loans rose by 6.8 per cent to 31,783, and first home buyers made up roughly one in three of all home purchases according to the Australian Bureau of Statistics. That matters because it tells you two things. First, demand from buyers like you is still strong. Second, the process is difficult enough that a clear plan matters more than hype.

Table of Contents

- Your Australian Dream A Realistic First Home Buyer Guide

- Check Your Eligibility and Government Grants

- Build Your Financial Foundation Deposit and Budget

- Unlock Your Loan With Mortgage Pre-Approval

- The Hunt Finding and Inspecting Properties

- Seal the Deal Offers Negotiations and Auctions

- The Final Stretch Contracts Conveyancing and Settlement

- The Smart Advantage How a Buyer's Agent Can Help

Your Australian Dream A Realistic First Home Buyer Guide

A good first home buyer guide shouldn't pretend this process is simple. It also shouldn't make it sound impossible.

Most buyers don't fail because they lack discipline. They struggle because the process rewards people who understand sequence. Check schemes before you set your target. Sort finance before you fall in love with a property. Inspect the building, not just the kitchen renovation. Negotiate with limits already decided, not in the heat of the moment.

That's where buyers often lose money. They treat buying as a search problem when it's really a decision problem.

Practical rule: The right first home is the one you can buy safely, hold comfortably, and still feel good about six months after settlement.

A realistic approach also means accepting trade-offs. Your first purchase may not be your forever home. It may be a townhouse instead of a freestanding house, or a stronger location with an older fit-out, or a smaller place that keeps your repayments manageable. In practice, buyers who accept that early usually move faster and make cleaner decisions.

What a solid plan looks like

A workable plan usually includes these parts:

- Scheme review first: Work out whether you qualify for grants, guarantees, or stamp duty relief before setting a suburb shortlist.

- Budget with buffers: Build your number around the full purchase, not just the deposit.

- Pre-approval before inspections: Sellers and agents respond differently when your finance is organised.

- Due diligence before emotion: Building, pest, zoning, flood, and surrounding development checks matter as much as the floorplan.

- Negotiation discipline: Decide your ceiling before the agent starts applying pressure.

That's how anxiety turns into action. You stop guessing, and you start making decisions in the right order.

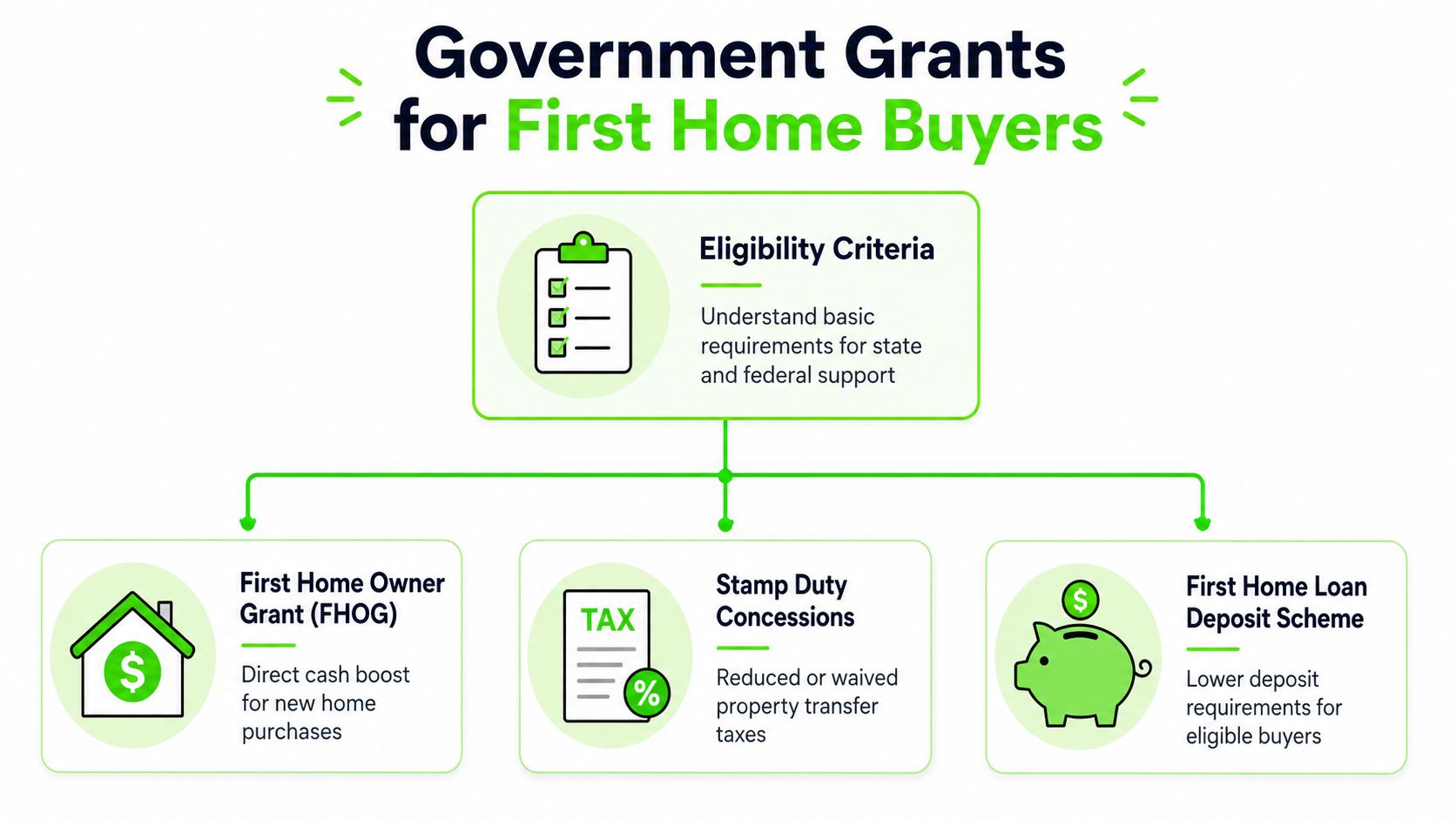

Check Your Eligibility and Government Grants

A lot of first home buyers get caught at the same point. They save hard, set a price range, start inspecting homes, then realise later they were eligible for support that could have changed the plan from day one.

That mistake is expensive. I've seen buyers overlook a stamp duty exemption worth tens of thousands, or assume a low-deposit government scheme works like a cash grant and budget incorrectly from the start. A buyer's agent should check this early, before suburbs, inspections, or offer strategy, because scheme eligibility can change what you can buy and how safely you can hold it.

Know the difference between a grant a concession and a guarantee

These are three different tools. Treat them differently.

| Type of support | What it does | Practical impact |

|---|---|---|

| Grant | Gives eligible buyers a direct payment | Reduces how much cash you need upfront |

| Stamp duty concession or exemption | Cuts or removes transfer duty | Preserves savings for legal fees, repairs, and buffer funds |

| Government guarantee scheme | Lets eligible buyers purchase with a lower deposit | Can help you buy sooner without paying lenders mortgage insurance in some cases |

The federal scheme many buyers ask about is the First Home Guarantee. It allows eligible buyers to purchase with a 5% deposit without paying LMI, subject to scheme caps and lender participation, according to the Housing Australia Home Guarantee Scheme. It is not a grant. No money lands in your account. It changes the deposit structure and, for the right buyer, shortens the time spent saving.

That distinction shapes your whole strategy. A cash grant helps with funds at settlement. A duty concession lowers transaction costs. A guarantee can get you into the market earlier, but it does not remove the need for repayment discipline, due diligence, or a cash buffer.

State support can materially change your numbers

State rules matter just as much as federal support, and they change often enough that buyers should verify them before making assumptions.

In South Australia, eligible first home buyers who build or buy a new home can access a $15,000 First Home Owner Grant, and stamp duty has been removed for eligible first home buyers buying a new home under the state's updated rules, as outlined by RevenueSA. For the right buyer, that can shift the decision between established and new property.

In New South Wales, eligible first home buyers purchasing a new home may receive a $10,000 First Home Owner Grant, and separate transfer duty relief may apply depending on the property and price, according to Revenue NSW. In Queensland, the First Home Owner Grant for eligible new homes is $30,000 for contracts within the current boosted period, according to the Queensland Revenue Office.

Those numbers are not just trivia. They affect whether you keep enough cash after settlement, whether a new build deserves a place on your shortlist, and whether your real limit is higher or lower than you first thought.

A buyer's agent adds value here by testing the trade-off, not just listing the schemes. A new townhouse with grant support and duty relief may beat an older apartment on total cost. The older property may still win on location, scarcity, or renovation upside. The right answer depends on your holding costs, commute, risk tolerance, and how long you expect to stay.

Check the hidden eligibility points before you rely on the money

Buyers often come unstuck. They read the headline benefit and miss the detail that controls whether they qualify.

Check these items first:

- Property type. Many grants apply to new homes, not established homes.

- Price caps. Federal and state schemes usually have strict purchase price limits.

- Occupancy rules. You generally need to live in the property for a minimum period.

- Applicant history. Prior ownership, even partial ownership, can affect eligibility.

- Timing. Contract dates, build commencement dates, and settlement timing can all matter.

I also tell buyers to review smaller transaction items early, including the deposit and earnest money rules when buying a home in Australia, because scheme eligibility does not protect you from a poorly structured contract or cashflow pressure at exchange.

If you are comparing a new build with an established property, look beyond the purchase incentives. Ongoing running costs can differ sharply. Some buyers also review programs such as the Australian solar battery rebate while weighing a more efficient new home against an older property that may need upgrades.

Grants help with cash. Concessions reduce transaction costs. Guarantees change deposit structure. Buyers who blur those lines usually misjudge their real budget.

Before speaking with a lender or making an offer, prepare a one-page eligibility checklist covering your state, property type, target price, occupancy plan, and timing. It sounds basic. It prevents expensive assumptions.

Build Your Financial Foundation Deposit and Budget

You find a place at $680,000. The repayments look manageable. Then additional costs start stacking up. Contract deposit, conveyancing, building inspection, lender fees, moving costs, a few repairs after settlement. Buyers get into trouble here, not because they cannot save, but because they build a purchase plan around the headline price and ignore the cash needed around it.

The 20% deposit rule is still useful. It usually gives you better loan options and keeps you clear of Lenders Mortgage Insurance. But plenty of first home buyers purchase with less than 20%, especially if they qualify for a government guarantee or have a strong income and stable savings history. Ultimately, the question is simpler. How much cash can you commit without leaving yourself exposed after settlement?

As a buyer's agent, I want clients to separate their budget into four clear buckets before they inspect a single property:

- Deposit funds. The amount going toward the purchase price.

- Purchase costs. Conveyancing, inspections, loan fees, transfer costs, and any upfront strata or title checks.

- Move-in costs. Removalists, cleaning, locksmiths, utility connections, and immediate furniture or appliance gaps.

- Cash buffer. Money left untouched for the first three to six months of ownership.

That last bucket gets neglected all the time.

A buyer with a 10% deposit and a $15,000 buffer is usually in a safer position than a buyer who empties every account to reach a bigger deposit and has nothing left for a hot water system, rate notice, or body corporate levy.

Build a budget around your life, not the lender's ceiling

Banks assess what they may lend. That figure is not a sensible spending target. I regularly see buyers approved for an amount that looks fine on paper and feels oppressive once real life is layered back in, especially if they are also paying childcare, car finance, or rising strata levies.

Use a tighter test:

- Start with available cash. Count savings you already hold and any family contribution that is confirmed, not discussed in vague terms.

- Set aside your emergency funds first. Do this before you decide what is available for the deposit.

- List transaction costs line by line. Do not rely on a rough guess.

- Add first-90-day ownership costs. Council rates, insurance, minor repairs, and basic maintenance often arrive quickly.

- Stress-test the monthly repayment. Check whether the number still works if rates rise, your fixed term ends, or one larger household expense lands at the wrong time.

A practical example helps. On a $700,000 purchase, a 10% deposit is $70,000. Add conveyancing, inspections, lender charges, moving costs, and an initial repair allowance, and many buyers need materially more cash than the deposit alone. If you are buying an apartment, review the strata records before you stretch to your ceiling. A building with low current levies can still hit owners with a special levy six months later.

Hidden due diligence that belongs in the budget stage

This is the part generic first home buyer guides usually skip.

Budgeting is not only about what you can borrow. It is also about what the property is likely to cost you once you own it. Older homes can need drainage work, rewiring, stumping, or a roof repair. Units can carry upcoming waterproofing works or lift replacement costs. Newer properties can look cheaper to run and still expose you to high owners corporation fees or defects.

I prefer buyers to cost these risks early. A building and pest inspection is not just a box to tick before exchange. It is part of budget control. The same goes for contract review, strata report analysis, flood checks, and council overlays where relevant. A buyer's agent helps here by cutting out stock that is cheap for a reason and keeping your search tied to the numbers you can live with.

Some buyers also get tripped up by overseas advice about commitment payments. Australian contracts work differently, but it still helps to understand how earnest money compares with Australian deposit rules so you know when cash is due and what happens if a deal falls over.

A first home budget should answer two questions. Can you buy it? Can you still handle the property comfortably after settlement?

That is the standard worth using.

Unlock Your Loan With Mortgage Pre-Approval

Pre-approval changes how you operate in the market. Without it, you're browsing. With it, you're in a position to act.

Agents can tell the difference straight away. So can sellers. A buyer who has spoken to a lender, prepared documents, and had their borrowing position assessed is usually taken more seriously than someone who says they'll “sort the finance later.” In a competitive campaign, that difference matters.

Why pre-approval changes your buying position

The technical side matters here. The absolute minimum deposit to secure a loan is 5% of the purchase price, but that typically requires a government guarantee to avoid Lenders Mortgage Insurance, and LMI is otherwise mandatory for deposits below 20% and can cost 2–3% of the loan value, according to Aintree Group. The same source states that the deposit must be personally saved over a 3-month period.

That “genuine savings” point catches buyers off guard. Sudden transfers, borrowed funds, or unexplained account movements can create friction. Pre-approval is where those issues should surface, not after you've committed emotionally to a property.

A clean pre-approval file usually includes:

- Income evidence: Payslips or other proof your lender accepts.

- Savings history: Statements showing where the deposit came from and how it accumulated.

- Debt clarity: Credit cards, personal loans, HECS or other liabilities.

- Expense realism: Living costs that reflect your life, not optimistic guesses.

Choose your loan structure by trade-off not by marketing

Loan choice is where buyers can get distracted by headlines. Keep it simple.

| Loan type | Main strength | Main trade-off |

|---|---|---|

| Fixed | Repayment certainty for a period | Less flexibility if rates or plans change |

| Variable | More flexibility and potential benefit if conditions move in your favour | Repayments can move |

| Split | Blends certainty and flexibility | More complexity to manage |

A fixed rate suits buyers who want payment predictability. A variable rate suits buyers who value flexibility and can tolerate movement. A split loan can work when you want part of the debt predictable and part flexible. None is universally “best.” The right fit depends on how stable your income is, how long you expect to hold the property, and how much volatility you can absorb without stress.

Pre-approval isn't a trophy. It's a working tool that tells you how to bid, where to look, and when to walk away.

The Hunt Finding and Inspecting Properties

Property hunting is where discipline gets tested. The photos are polished, the copy is optimistic, and a crowded open home can make an average property feel rare.

The mistake I see often is buyers inspecting homes as future owners before they inspect them as risk managers. You need both lenses. One tells you whether you want to live there. The other tells you whether you should.

Two buyers two very different outcomes

Take two common first-home scenarios.

Buyer one falls for presentation. Fresh paint, new tapware, nice furniture, strong turnout at the open. They assume the property must be fine because everyone else seems keen. They skip or rush the deeper checks.

Buyer two likes the same property but stays methodical. They organise a building inspection and a pest inspection. They review council and location issues. They ask whether the home sits in an area with planning changes, flood or fire concerns, or nearby development that could affect future use and value.

That second buyer is handling risk properly. A rigorous pre-purchase due diligence protocol requires both a general building inspection and a pest inspection, and hidden structural defects can cost $50,000–$200,000+ to remediate, while buyers who complete those steps reduce risk exposure by 70–80%, according to St.George's first home buyer guide.

If you want a more detailed breakdown of what those reports cover, this guide to building and pest inspection is a useful companion before you book inspections.

Read beyond the styling and the sales pitch

When you inspect a property, pay attention to what can't be solved with cushions and staging.

Look for signs like these:

- Movement clues: Uneven flooring, cracks that suggest more than cosmetic settlement, doors that don't close cleanly.

- Moisture issues: Musty smells, staining, roofline irregularities, poor ventilation in wet areas.

- Layout compromises: Bedrooms off living zones, poor natural light, awkward parking, difficult access.

- Location realities: Main-road noise, overshadowing, neighbouring construction, drainage patterns, and school catchment implications.

A buyer's agent can be useful here because they tend to inspect with detachment. They're less likely to be distracted by paint colour and more likely to notice what will affect value, livability, and resale. That matters for first home buyers because your first property often becomes your future stepping stone.

Seal the Deal Offers Negotiations and Auctions

By the time you're ready to buy, the process usually splits in two directions. Private treaty or auction. They require different tactics, different emotional control, and a different level of legal readiness.

Treat them as two separate games. Buyers who don't usually overpay in one or freeze in the other.

Private treaty gives you room to protect yourself

Private treaty is the more flexible path. You review the contract, make an offer, negotiate on price and terms, and often have room to include conditions that protect you.

That flexibility can help first home buyers in several ways:

- Finance condition: Useful when your formal approval still needs to catch up.

- Building and pest condition: Gives you a path to renegotiate or exit if serious issues appear.

- Settlement timing: Can be adjusted to suit your lender, tenancy arrangements, or practical move dates.

Private treaty also tends to reward patience and information. A strong offer isn't always the highest opening number. Sometimes it's the cleanest overall package. Good communication through your solicitor or conveyancer, clarity on timing, and proof that your finance is organised can make your position more attractive.

In a private treaty negotiation, certainty can be as persuasive as money.

Auction demands preparation and emotional control

Auction is a sharper environment. Once the hammer falls, the purchase is generally unconditional. That means your finance, due diligence, and contract review need to be done before auction day, not after.

The discipline here is simple and hard:

- Set your ceiling before the auction.

- Decide who will bid.

- Ignore the theatre.

- Stop when the number passes your limit.

Vendor bids, fast increments, and crowd energy can make buyers detach from their original plan. That's where many first home buyers get hurt. They stop buying a property and start trying to win an event.

A practical comparison helps:

| Method | Main advantage | Main risk |

|---|---|---|

| Private treaty | More room for conditions and negotiation | Buyers can drift or negotiate against themselves |

| Auction | Clear time frame and visible competition | Emotion can override discipline and contracts are typically unconditional |

A buyer's agent often adds the most visible value at this point. They can read agent behaviour, judge when a campaign is running hot or soft, and keep your bidding detached from ego. Even if you bid yourself, use a written maximum and a written walk-away rule. Verbal limits get softer when the auctioneer speeds up.

The Final Stretch Contracts Conveyancing and Settlement

An accepted offer feels like the hard part is over. It isn't. It's the point where legal detail, lender timing, and final checks matter most.

This period is where experienced buyers stay calm and first home buyers often feel like things have gone suddenly quiet. In reality, a lot is happening. Your conveyancer or solicitor is reviewing documents, the lender is moving the loan toward final approval, and both sides are working toward settlement.

What happens after your offer is accepted

The broad sequence usually looks like this:

- Contracts are signed and exchanged.

- Your deposit is paid in line with the contract.

- Conveyancing work begins.

- Your lender completes final steps.

- You conduct a pre-settlement inspection.

- Settlement occurs and ownership transfers.

Your conveyancer or solicitor is there to protect your side of the transaction. They review the contract, manage legal correspondence, coordinate with the seller's representative, and help ensure the title transfer and settlement process happen properly. If a special condition matters to you, this is not the stage for assumptions. Get it checked and confirmed in writing.

Use the pre-settlement inspection properly

The pre-settlement inspection isn't a courtesy walk-through. It's a final verification.

Check that the property is in the agreed condition, inclusions remain in place, and no material issue has emerged since exchange. If something's changed, raise it immediately through your legal representative. Don't collect the keys and hope it gets fixed later.

It also helps to plan the practical side of move-in before settlement day lands on you all at once. Buyers often line up cleaners, utilities, internet, and access arrangements during this final stage. If you want a realistic sense of service scope and timing, reviewing move in cleaning pricing can help you budget for that handover period properly.

Settlement day is mostly administrative from your side, but emotionally it's big. Once funds are exchanged and the transfer is completed, the keys are released. That's the point where the whole process stops being theoretical.

The Smart Advantage How a Buyer's Agent Can Help

A first home buyer often loses money long before settlement. It happens in the search, in the reading of price guides, in the choice to chase the wrong stock for six weekends, or in the split-second decision to stretch because the kitchen looks good under open home lighting.

That is why a good buyer's agent adds value across the whole process, not only at offer stage. The job is part strategist, part filter, part negotiator. For first home buyers, a significant benefit is having someone on your side who can separate a suitable property from an expensive lesson.

A capable agent starts by pressure-testing the brief. In practice, that means asking harder questions than many buyers ask themselves. Is a lower-maintenance townhouse a better first step than a freestanding house 20 kilometres further out? Is the suburb you like workable once commuting, strata costs, flood exposure, and resale demand are factored in? Is a property still affordable after stamp duty, legal fees, building inspections, and immediate repairs?

During the search, they bring a more commercial lens to the decision:

- Value assessment: reading past the sales pitch and judging whether the asking range is supported by recent comparable sales

- Risk spotting: identifying issues with layout, location, strata records, renovation quality, or surrounding development that deserve closer review

- Selling agent feedback: interpreting what the campaign is signalling about buyer competition, vendor motivation, and likely price expectations

- Negotiation approach: deciding whether to move early, wait, go hard pre-auction, or hold your line and let a poor listing campaign work in your favour

If you are still clarifying the role itself, this guide on what a buyer's agent does in an Australian property purchase gives a clear overview.

The hidden advantage is judgment under pressure. I see first home buyers get into trouble when they become attached before they have done the boring checks properly. A buyer's agent can slow the process down at the right moment, ask for the strata report, query the contract terms, challenge an optimistic price guide, or tell you to walk away when the compromise is too big. Detached judgement saves buyers from forcing a bad deal.

That matters most in the moments buyers remember clearly. Auction day. A best-and-final offer round. A building report that uncovers moisture, movement, or unapproved works after you have already planned where the couch will go. The right adviser does not just help you buy property. They help you reject properties that do not stack up.

There is also a time trade-off. Buyers can absolutely purchase without an agent, and plenty do. But if you are balancing full-time work, finance deadlines, inspections, suburb research, and negotiation with experienced selling agents, paying for representation can be a rational decision rather than a luxury. The calculation is simple. If better selection, tighter negotiation, and fewer mistakes save you from overpaying or buying the wrong asset, the fee can make sense.

If you are already thinking beyond exchange and settlement, a practical 2025 ultimate moving guide can help you organise the move without leaving everything to the final week.

A short explainer is useful here before making that call:

The right first home buyer guide should leave you with a framework, not just encouragement. Used properly, a buyer's agent gives you structure, sharper due diligence, and a steadier hand through one of the biggest financial decisions you will make.

If you want experienced support through suburb selection, due diligence, negotiation, and the full buying process, speak with the team at We Are Buyers Agents. They work with Australian buyers from strategy through to purchase, which can be especially valuable when you're buying your first home and want a clear plan rather than guesswork.