You're probably in one of two positions right now. You've either spent weeks scrolling listings, turning up to inspections, second-guessing every suburb and every floor plan, or you're trying to buy from a distance and you know that one bad call can lock you into years of underperformance. Both situations feel expensive, just in different ways.

That's where investment property services stop being a vague industry phrase and start becoming practical. A good buyer's agent doesn't just “help you buy”. They build the brief, filter the noise, test the numbers, inspect the downside, negotiate the terms, and keep the whole process moving so you don't overpay for the wrong asset.

For investors looking at Sydney and Byron Bay, the difference matters. These are not markets where generic advice works. Sydney punishes indecision and sloppy due diligence. Byron Bay punishes buyers who confuse lifestyle appeal with investment logic. If you want a property that performs, not just one that photographs well, you need process, discipline, and local judgement.

Table of Contents

- Tired of Missing Out on Investment Properties?

- The Full Spectrum of Investment Property Services

- Your Investment Journey with a Buyer's Agent

- Understanding Fees and Calculating Your Return on Investment

- Navigating the Sydney and Byron Bay Property Markets

- Real-World Success Stories and Investment Examples

- Your Checklist for Choosing the Right Buyer's Agent

Tired of Missing Out on Investment Properties?

A lot of first-time investors think the hard part is finding a property. It usually isn't. The hard part is knowing which property to ignore.

In Sydney, I regularly see buyers spend entire Saturdays moving from one open home to the next, only to end the day with more confusion than clarity. One apartment looks cheap until you compare the strata exposure. One terrace looks “full of potential” until you assess what the renovation path really involves. One auction guide looks manageable until the bidding starts and the campaign has already reset the market's expectations.

That's the point where DIY buying starts to cost more than it saves.

What most buyers are really fighting

You're not just competing with other buyers. You're competing with selling agents who know how to create urgency, investors who already understand their buy box, and experienced operators who can identify weak stock in minutes. If your process is reactive, you'll keep feeling late.

A buyer's agent changes that balance. Instead of turning up cold to a polished sales campaign, you work from a strategy. Instead of assessing a property in isolation, you assess it against your target yield, likely holding costs, asset quality, tenant appeal, and exit options.

“The first loss in property is usually made at the time of purchase.”

That line appears often in the financial press because it's true in practice. If you buy the wrong asset, your property manager, accountant, and mortgage broker can only do so much after the fact.

What a strategic advantage looks like

Good investment property services give you structure where most buyers rely on instinct.

- A sharper brief: You stop looking at “anything under budget” and start targeting assets that fit a clear plan.

- Cleaner decision-making: You compare opportunities on fundamentals, not sales language.

- Better negotiation footing: You're not working out your ceiling while the other side is already working your emotions.

- Less hidden risk: Problems in title, building condition, tenancy profile, location quality, or future spend get surfaced earlier.

I've watched plenty of capable professionals struggle when they buy alone. Not because they aren't smart, but because property buying rewards repetition, local pattern recognition, and disciplined execution. Most investors don't need more listing alerts. They need someone whose job is to protect the downside while hunting for the upside.

The Full Spectrum of Investment Property Services

A buyer's agent for investors is best thought of as your personal property department. You're not hiring one skill. You're hiring a chain of decisions that have to hold together from brief to settlement.

What sits inside the service

The first job is strategy. That means defining the target asset, location style, risk tolerance, and intended outcome. Some investors want cleaner cash flow. Others will tolerate a tighter starting position for a better long-term hold. Without that clarity, every listing looks half-right.

Next comes search and access. That includes on-market screening, agent relationships, pre-market conversations, and eliminating unsuitable stock before it wastes your time. In these efforts lies much of the value. Buyers often think they need more options. In reality, they need fewer, better-filtered options.

Then comes assessment. At this stage, investment property services become technical rather than promotional.

| Service pillar | What it does in practice | Why it matters |

|---|---|---|

| Brief development | Defines suburbs, asset type, budget guardrails, risk profile | Stops random buying |

| Sourcing | Screens listings, agent networks, pre-market and off-market leads | Improves opportunity flow |

| Due diligence | Reviews location, building, comparables, rentability, likely costs | Reduces expensive surprises |

| Valuation and negotiation | Tests price logic and handles offer strategy | Protects entry point |

| Settlement coordination | Keeps broker, solicitor, and agent aligned | Prevents process friction |

Why the pieces have to work together

Inexperienced buyers often break the chain. They might research suburbs well but negotiate poorly. Or negotiate firmly but skip proper due diligence. Or buy a decent asset and then fail to line up the right manager and tenancy plan.

Practical rule: A property only works as an investment when the acquisition logic, the numbers, and the operational plan all agree.

For remote buyers and interstate investors, this joined-up approach matters even more. Content in the market often underplays how difficult it is to assess ageing properties in underserved areas without a full-service local partner. Research on that segment found 68% of retail investors shifting to underserved areas report inadequate due diligence on physical asset conditions, leading to unexpected stabilization costs averaging $45,000 per property in NewMark Merrill's discussion of underserved-market investing.

That's one reason many buyers now want a more structured acquisition process. If you want a clean view of how that process runs from first brief to settlement, this stress-free property buying checklist from brief to settlement gives a useful operational frame.

A full service also includes referrals and coordination. Solicitors, finance brokers, strata inspectors, building inspectors, depreciation specialists, and property managers all affect the result. A buyer's agent doesn't replace them. They make sure their work points in the same direction.

Your Investment Journey with a Buyer's Agent

The client experience should feel structured, not theatrical. If the process feels improvised, that's usually a warning sign.

Early on, the primary work is diagnosis. The investor says they want “a good property in a growth area”, but that's not actionable. The brief gets sharpened into purchase range, asset type, cash flow tolerance, preferred hold period, and whether flexibility matters for future owner-occupier use. That first stage saves a huge amount of wasted effort later.

Here's the process visually before we get into the detail.

How the process usually unfolds

A clean acquisition path tends to follow this order:

Initial strategy call

Budget, borrowing position, purchase timing, target geography, and investment goals get defined.Search and shortlisting

Suitable properties are filtered in. Unsuitable stock is ruled out quickly. That includes properties that are overpriced, compromised, or hard to hold well.Inspection and analysis

The shortlist gets pressure-tested. Rentability, layout, building quality, comparable sales, and negotiation angle all matter here.Offer or bidding strategy

Some properties should be pursued early. Others are worth taking to auction. Others should be left alone.Contract and settlement management

Broker, solicitor, inspector, and selling agent all need coordination. Delays often happen when nobody owns the process.Post-settlement handover

Leasing preparation, manager introduction, and hold strategy should be lined up before settlement, not after.

A lot of clients want to understand the role more clearly before they engage anyone. This plain-English guide on what a buyer's agent does is useful for that.

Later in the process, communication becomes as important as research. Good agents don't flood you with property links. They send a smaller set of considered options and tell you why each one made the cut, what the risks are, and what decision is required next.

Where remote buyers gain the most

Remote purchasing is where modern systems stop being optional. Buyers need access to virtual tours, digital document review, real-time updates, and clean financial reporting. That isn't a luxury feature anymore. It's part of competent execution.

The market data on this is clear. 72% of remote investors report difficulty finding service providers with integrated technology platforms for virtual tours, real-time performance tracking, and digital tenant communication in Sunworld Group's sight-unseen property investment analysis.

That's why many buyer's agents now rely on a stack of practical tools, not just phone calls. Virtual inspections, shared due diligence folders, digital contract workflows, and property management platforms such as AppFolio or Yardi help keep financial and operational details visible. For remote clients, that visibility often determines whether they feel confident enough to act.

This short video gives a useful sense of how the buying journey can be managed in a more structured way.

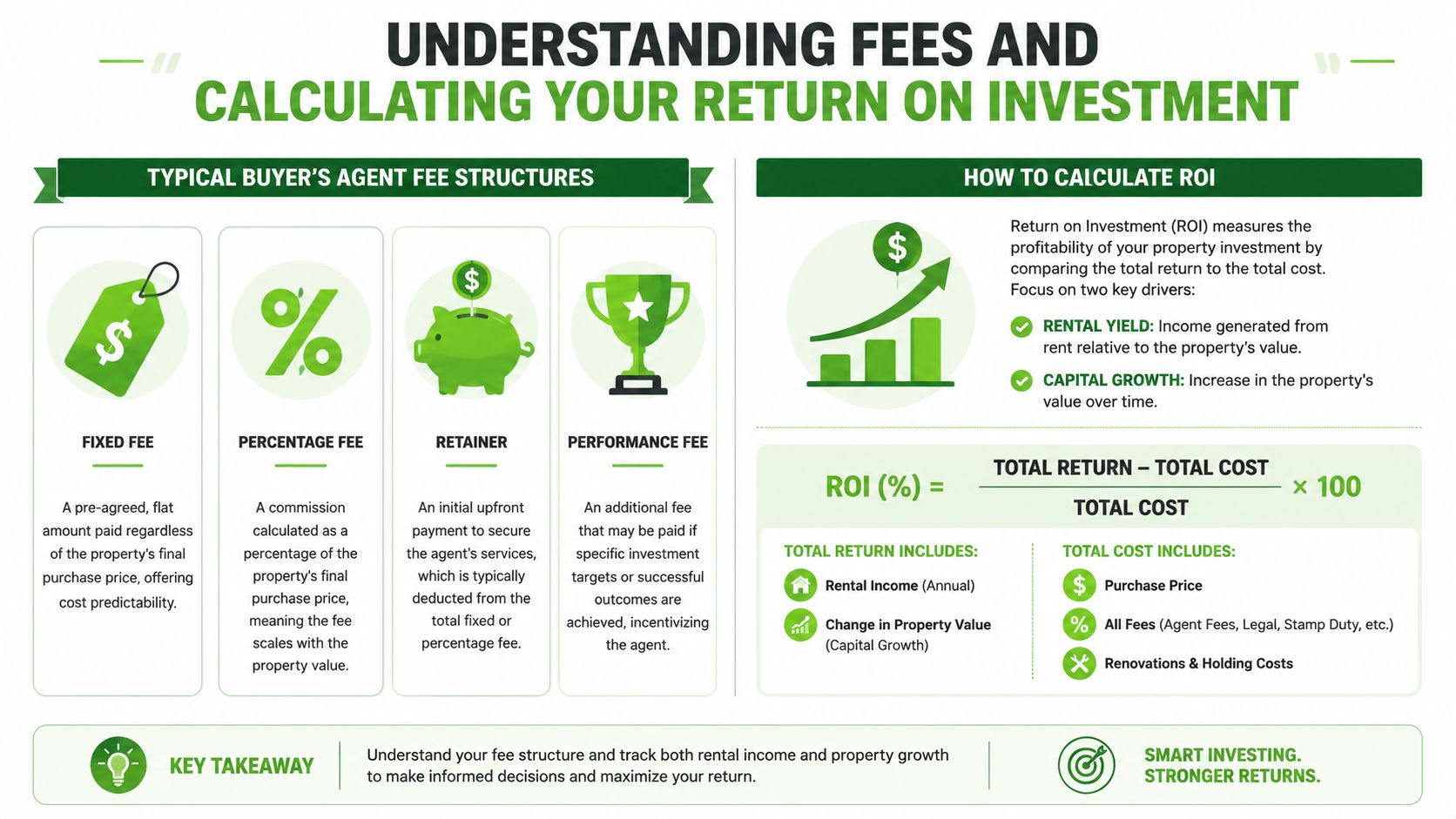

Understanding Fees and Calculating Your Return on Investment

A client buys a Sydney investment property for $1.85 million, then spends the next two years carrying avoidable costs because no one picked up the weak strata position, the inflated campaign pricing, or the rental limitations in the floor plan. The buyer's agent fee would have been visible on day one. The cost of a poor purchase only shows up later, through lower yield, extra capital works, longer vacancy, and slower growth.

That is the right frame for this conversation. Fees matter, but the main question is whether the service improves the investment result by more than it costs.

How fee structures work

Buyer's agents usually charge in one of four ways. Fixed fee, percentage of purchase price, a retainer that forms part of the total, or a hybrid with a result-based component. None is automatically better. The right structure depends on the brief, price point, and how clearly the service scope is defined.

Here is how I explain the trade-offs to clients:

- Fixed fee: Clear budgeting from the start. Often suits investors who want cost certainty and expect a focused brief.

- Percentage fee: Moves with the purchase price. Some clients accept that if the search range may shift during the engagement.

- Retainer model: Common when the brief is urgent or broad and work starts immediately.

- Performance-linked fee: Works only if the success measure is specific, documented, and realistic.

The fee format is less important than the engagement terms. You should know what is included, what is excluded, when invoices are raised, whether auction bidding sits inside the fee, and whether due diligence, negotiation, and post-settlement support are part of the mandate.

What return actually looks like

The return on a buyer's agent is rarely one dramatic discount. It usually comes from a series of disciplined decisions.

Paying $70,000 less than the emotional bidder at auction matters. Avoiding a block with major remedial works matters more. Buying a property that rents faster, attracts stronger tenants, and needs fewer corrections in year one often has the best financial impact of all.

In Sydney, that can mean rejecting a polished apartment in a high-fee complex and choosing a less flashy asset with better rental depth and lower holding risk. In Byron Bay, it can mean walking away from a short-stay candidate that looks attractive on gross income but becomes far less appealing once cleaning, changeover, platform, and local management costs are added in. Before you assume the holiday-let model will outperform, it helps to determine your Airbnb management fees and compare the net result with a standard lease.

A simple ROI check should cover more than purchase price alone:

- entry price relative to fair market value

- likely rent and vacancy risk

- strata, maintenance, and capital works exposure

- financing impact from buying above or below appraisal support

- resale appeal in a normal market, not just a hot one

For investors comparing options suburb by suburb, a proper rental market analysis for the target area gives a better basis for decision-making than broad city averages.

A practical way to judge value

If a buyer's agent fee is $20,000 and the agent helps you avoid overpaying by $40,000, the fee has already paid for itself. If they also steer you away from a property with weak tenant appeal or hidden building costs, the return improves again. Some value is immediate. Some shows up over the hold period.

That is why I tell clients to judge fees against three outcomes. Purchase quality, risk reduction, and time saved. Time matters because missed opportunities have a cost too, especially in tightly held Sydney pockets where hesitation can mean chasing the market upward for another six months.

Good advice is not cheap. Bad asset selection is usually far more expensive.

Navigating the Sydney and Byron Bay Property Markets

Sydney and Byron Bay both attract committed buyers. They require very different judgement.

Sydney is a scale market. There are more transactions, more micro-markets, more competing buyer profiles, and more situations where the sales campaign itself distorts the buyer's view of value. Byron Bay is narrower and more emotional. A buyer can overpay there by falling in love with a street, a mood, or a future holiday-use idea that doesn't hold up once the ownership realities kick in.

Sydney requires financial discipline

In Sydney, I care less about the headline story and more about the property's operational logic. Is the layout rentable? Is the building likely to absorb capital? Does the location support tenant depth? Does the price still work after you strip out campaign heat?

For multifamily-style analysis, a benchmark Net Operating Income yield of 4.5% to 5.2% in major markets like Sydney indicates a healthy asset, while yields below 3.8% often signal overvaluation in the benchmark summary captured in this Sydney NOI yield market query. That framework is useful because it forces discipline. A property can look fashionable and still fail the numbers.

For investors comparing suburbs or rental demand patterns, a proper rental market analysis is more useful than broad metro commentary. Tenant appeal in one Sydney pocket can look very different a few train stops away.

Local rule: In Sydney, the asset usually beats the suburb headline. A mediocre property in a fashionable postcode can still underperform.

Byron Bay requires risk filtering

Byron Bay asks different questions. You're assessing not just the asset and the tenant profile, but also how lifestyle demand interacts with local constraints. Holiday-letting assumptions can mislead buyers. So can maintenance on coastal stock, neighbourhood character, and the gap between “great for a week” and “great to own for years”.

Often, generic investment property services fall short. The buyer doesn't need another description of “strong demand”. They need someone to say whether the property is sound, manageable, and suitable for the ownership model they want.

I also see more mixed-purpose buying in Byron Bay. Some clients want a future home with present investment utility. Others want an income property that won't become a management burden. That's fine, but it only works when those aims are acknowledged early. A confused brief creates a compromised purchase.

Real-World Success Stories and Investment Examples

A Sydney investor sees three decent listings on Thursday, inspects two on Saturday, and is ready to offer on the one that feels safest by Sunday night. That is often the point where money is either protected or wasted. The difference usually comes down to whether the buyer is judging the property by pressure and presentation, or by numbers, risk, and resale depth.

The Sydney investor

A common Sydney brief is straightforward on paper. The client has income, borrowing capacity, and a clear intent to buy, but too little time to assess every trade-off properly. After a month or two, the search often becomes reactive. They start comparing polished apartments across very different buildings and micro-markets, and the wrong property begins to look acceptable, solely due to its availability.

The financial value of good advice shows up before purchase. I will often rule out a property that photographs well and rents quickly because the strata is too high, the floor plan limits future owner-occupier demand, or the building carries defects risk that could affect both hold costs and resale. Passing on that asset can save far more than the buyer's agent fee.

I have seen this play out with inner and middle-ring Sydney apartments in particular. One property may be $35,000 cheaper but come with higher levies, weaker natural light, poorer layout, and a tenant profile that turns over more often. Another may cost more upfront and still be the better investment because vacancy risk is lower, rent growth has more room, and resale appeal extends beyond investors. That is the kind of trade-off that improves the result over five to ten years, not just on contract day.

Cash flow briefs need a different filter. If a client wants the property leased fast and managed without constant intervention, I focus on rent readiness, realistic leasing evidence, likely maintenance, and whether the yield works after the actual costs of ownership, not just the headline rent. A high gross yield can still produce a mediocre investment if repairs, strata, insurance, or tenant churn eat into the return.

The Byron Bay lifestyler

Byron Bay buyers usually arrive with a blended brief. They want a property they can enjoy, hold with confidence, and potentially rent without creating an operational headache. The risk is paying a premium for a feeling rather than for durable value.

A house can have privacy, charm, and strong holiday appeal but still be a poor long-term investment if the maintenance load is heavy, access is awkward, the layout limits tenant demand, or the ownership costs are out of line with the likely income. Coastal stock can be expensive to maintain. Lifestyle buyers sometimes underestimate that in the excitement of securing the right setting.

The better Byron outcomes come from ranking priorities early. If capital preservation matters most, the search should favour scarcity, usability, and broad resale demand. If part-time personal use matters most, the numbers need to be tested against that reality instead of stretched to justify the purchase. Mixed motives are fine. Unclear motives are expensive.

I also find that buyers get better results when acquisition and management are treated as one decision, not two separate tasks. That is one reason specialist support keeps growing across mature property markets. Analysts at IBISWorld's property management industry overview describe a large, established management sector in the U.S. The local lesson is simple. Ownership now involves more moving parts, and investors who coordinate buying, leasing, maintenance, and risk control from the start usually make fewer costly mistakes.

Your Checklist for Choosing the Right Buyer's Agent

A poor buyer's agent decision is expensive in ways investors usually notice too late. It can mean chasing the wrong suburbs, overpaying under auction pressure, buying stock with weak tenant appeal, or spending weeks on properties that should have been ruled out in ten minutes. The right adviser reduces those errors and improves the odds of buying an asset that performs on both cash flow and resale.

In Sydney, that often comes down to whether they can separate a good street from a good investment. In Byron Bay, it often comes down to whether they understand the ownership costs, tenant profile, and resale depth behind the lifestyle appeal. Different market, same test. Can they protect your capital while still buying something that fits your brief?

Questions worth asking upfront

Ask questions that expose their decision-making, not their sales pitch.

- What suburbs and asset types do you buy most often? Look for clear examples. A buyer's agent who knows Sydney's inner west may not be the right fit for Byron's coastal villages, and vice versa.

- What makes you rule a property out? Good agents reject a lot of stock. I pay close attention to this answer because exclusions usually reveal whether they are disciplined or just optimistic.

- How do you assess investment performance before making an offer? They should be able to explain yield, comparable sales, likely tenant demand, downside risks, and resale liquidity in plain language.

- What does your due diligence cover? Ask about strata review, building issues, flood or bushfire exposure where relevant, renovation risk, and local supply that could affect rents or future buyer demand.

- How do you handle conflicts of interest? The answer should be direct. You want to know who pays them, whether they accept referral fees, and whether they ever represent the selling side.

- What is included in your fee? Clarify whether the scope covers strategy, search, inspections, appraisal, negotiation, auction bidding, and post-exchange support.

- Who do you coordinate with during the purchase? A good result often depends on timing between broker, solicitor, building inspector, strata inspector, and property manager.

- How do you report back to clients? Clear updates matter, especially in competitive Sydney campaigns where decisions need to be made quickly.

A practical example is We Are Buyers Agents, a Sydney and Byron Bay buyers agency that handles strategy, search, due diligence, negotiation, and acquisition support. The pertinent question is whether the scope, process, and market focus match the way you want to buy.

A few practical FAQs

| Question | Short answer |

|---|---|

| Can a buyer's agent help at auction? | Yes. Many investors hire one for bidding discipline, price limits, and pre-auction negotiation. |

| Can they help with investment properties and homes to live in? | Yes, but the buying criteria should change. A home purchase can justify compromises that an investment should not. |

| Do they replace a solicitor or broker? | No. They work alongside them and help keep the process coordinated. |

| Is doing it yourself cheaper? | Sometimes on paper. Not if you overpay, buy poor-quality stock, or lose time chasing unsuitable properties. |

The labour market gives a useful reality check. The median annual wage for property, real estate, and community association managers in the United States was $66,700 in May 2024 according to the U.S. Bureau of Labor Statistics occupational profile. That figure does not price an Australian buyer's agent service, but it does show that skilled property work carries real economic value.

One clear warning sign stands out.

If an agent can't explain their process clearly before you engage them, don't expect clarity once money is on the line.

A capable buyer's agent gives you more than access to listings. They sharpen the brief, cut away poor fits early, test value against evidence, and keep emotion from driving the number you pay. For a Sydney investor buying under competition, or a Byron Bay buyer balancing yield against holding costs, that can be worth far more than the fee.