You've probably reached the point where the first property decision felt straightforward, but the second one doesn't.

A common version of it looks like this. You live in Sydney, you've built equity in your home, your income is stable, and now you're weighing two very different purchases. One is a holiday house in Byron Bay that your family will use. The other is a pure investment in a Sydney suburb where tenants, yield, and long-term capital growth drive the decision.

Both can be smart. Both can also become expensive mistakes if you buy the wrong asset for the wrong reason.

The issue isn't just preference. In Australia, the same property can be treated very differently depending on whether you use it personally or buy it mainly to produce income. That affects how lenders assess the loan, how the ATO treats deductions, how you handle CGT, and how much ongoing management you're really signing up for. Industry commentary also notes that the decision to buy for personal use versus rental income places the buyer into two distinct categories for tax and lending purposes, and that the same dwelling can be treated very differently depending on occupancy and income intent in Australian rules, as discussed by Team Banx on second homes and investment properties.

Table of Contents

- The Great Australian Property Dilemma

- At a Glance Key Differences

- The Tax Implications A Deep Dive into ATO Rules

- Financing and Lender Criteria

- Cash Flow Scenarios Sydney vs Byron Bay

- Lifestyle Strategy and Ownership Rules

- Making Your Final Decision A Checklist

The Great Australian Property Dilemma

A Sydney buyer with strong borrowing power usually asks some version of the same question. Should I buy an asset that improves my balance sheet, or should I buy a place I want to spend time in?

If you're looking at a two-bed apartment in Marrickville, the thinking is usually clean. You care about tenant demand, transport, strata quality, and whether the numbers stack up after interest, rates, and management fees. If you're looking at Byron Bay, the thinking gets messier. You start with lifestyle, then try to make the economics behave.

That's where buyers confuse themselves. A Byron property can look like an investment because it may earn rent for part of the year. A Sydney investment can look flexible because you might one day move into it. But the practical question is simpler than that. What is the property for on day one?

Practical rule: If you need rental income and tax deductibility to justify the purchase, treat it as an investment decision from the start.

In my experience, the cleanest outcomes come when the use case is honest. Buyers who say, “This is a family asset first, and I'm comfortable carrying it,” usually make better second-home decisions. Buyers who say, “This needs to work financially even if I never use it,” are usually better suited to an investment property.

The trouble starts when someone wants full lifestyle access, strong holiday income, broad tax deductions, and owner-style lending terms all at once. That combination rarely holds together cleanly.

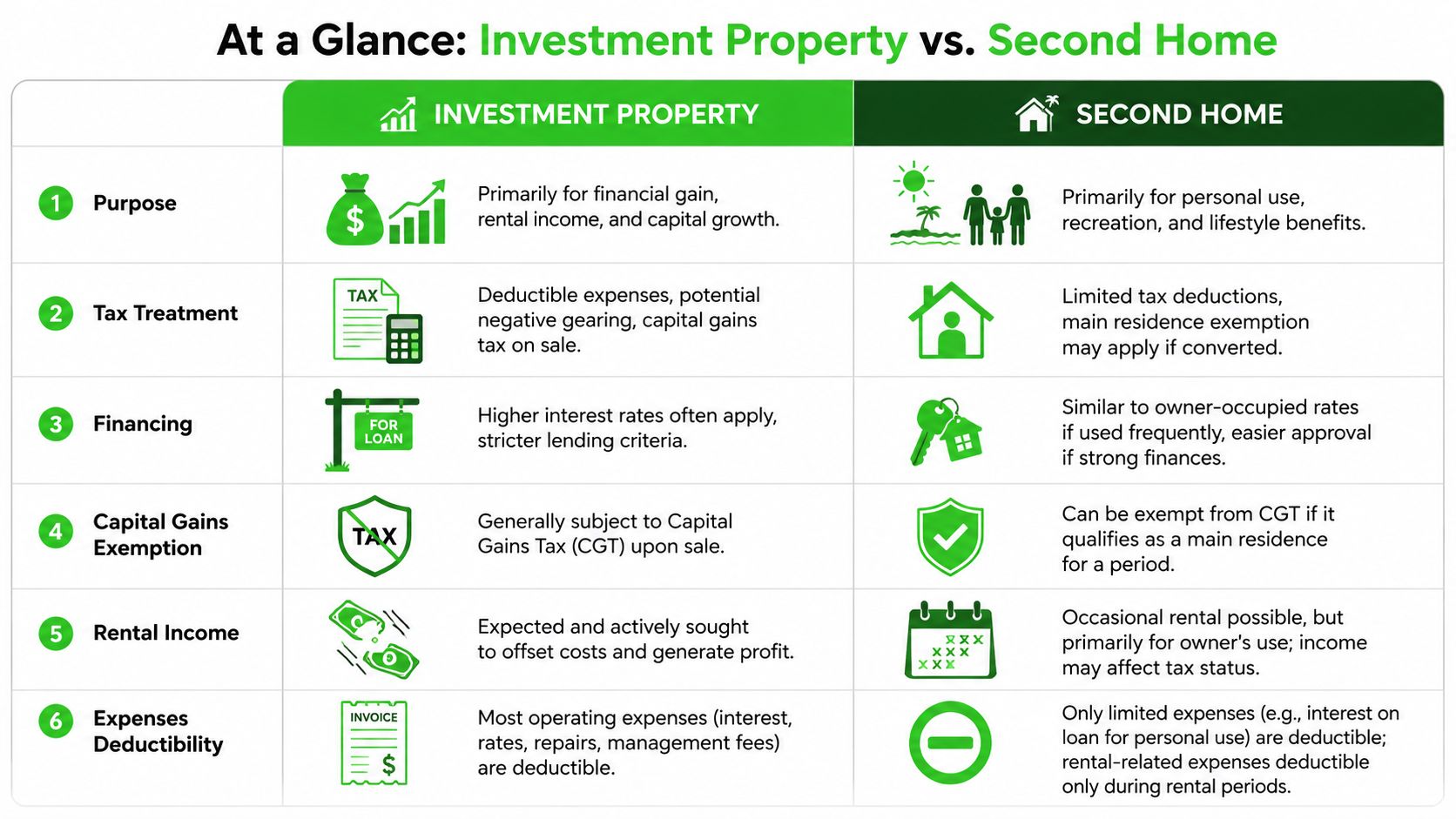

At a Glance Key Differences

An investment property and a second home can look similar on a listing portal. On the ground, they behave very differently once you factor in ATO treatment, lender policy, carrying costs, and how often you plan to use the place yourself.

At a Glance Investment Property vs Second Home

| Criterion | Investment Property | Second Home (Holiday Home) |

|---|---|---|

| Primary purpose | Rental income, capital growth, long-term wealth building | Personal use, family holidays, lifestyle flexibility |

| Tax treatment | Expenses may be deductible where they relate to earning assessable rental income, subject to normal ATO rules | Private use usually restricts deductions. Any claim depends on rental availability, actual income use, and apportionment |

| CGT position | Usually treated as an investment asset on sale, with CGT applying subject to ownership structure and holding period | Depends on how the property was used over time and whether any main residence treatment is available |

| Lending view | Banks usually assess it as higher risk and shade rental income | Can be assessed more favourably than an investment property if the borrower can show genuine personal use and strong servicing |

| Deposit expectation | Buyers should plan for stricter lending settings and less generous policy than an owner-occupied purchase | Often easier to position with a lender than a pure investment, but the file still needs to make sense on income, liabilities, and intended use |

| Income expectation | The numbers need to work with rent as part of the case | Rent is often incidental, seasonal, or not part of the decision at all |

| Management load | Leasing, compliance, arrears, repairs, property manager oversight | Cleaning, short-stay turnover, vacant periods, personal maintenance, and heavier wear during peak seasons |

| Typical buyer mindset | “Will this property perform in my portfolio?” | “Will my family use it enough to justify the annual cost?” |

In Sydney, that often means a buyer treats a Marrickville or Parramatta apartment as a numbers exercise first. In Byron Bay, the same buyer may accept weaker yield because access, lifestyle, and scarcity matter more than weekly rent.

That difference matters early. It affects borrowing strategy, expected holding costs, and even whether purchase expenses should be viewed through an income-producing lens. Buyers often miss that acquisition costs are not all treated the same way, which is why it helps to understand the tax treatment of conveyancing fees in Australia before you buy.

If you want a quick primer before getting deeper into structure and strategy, this explainer on what is investment property is a useful companion read because it frames the income-first mindset clearly.

Use this shortcut:

- Choose an investment property if the property needs rental income, tax deductions, and resale performance to justify the purchase.

- Choose a second home if you are comfortable funding a lifestyle asset that may not stack up like a Sydney investment.

- Treat mixed-use properties carefully if you want both personal access and holiday income, because that is where borrowing, deductions, and CGT treatment often become less favourable and more complex.

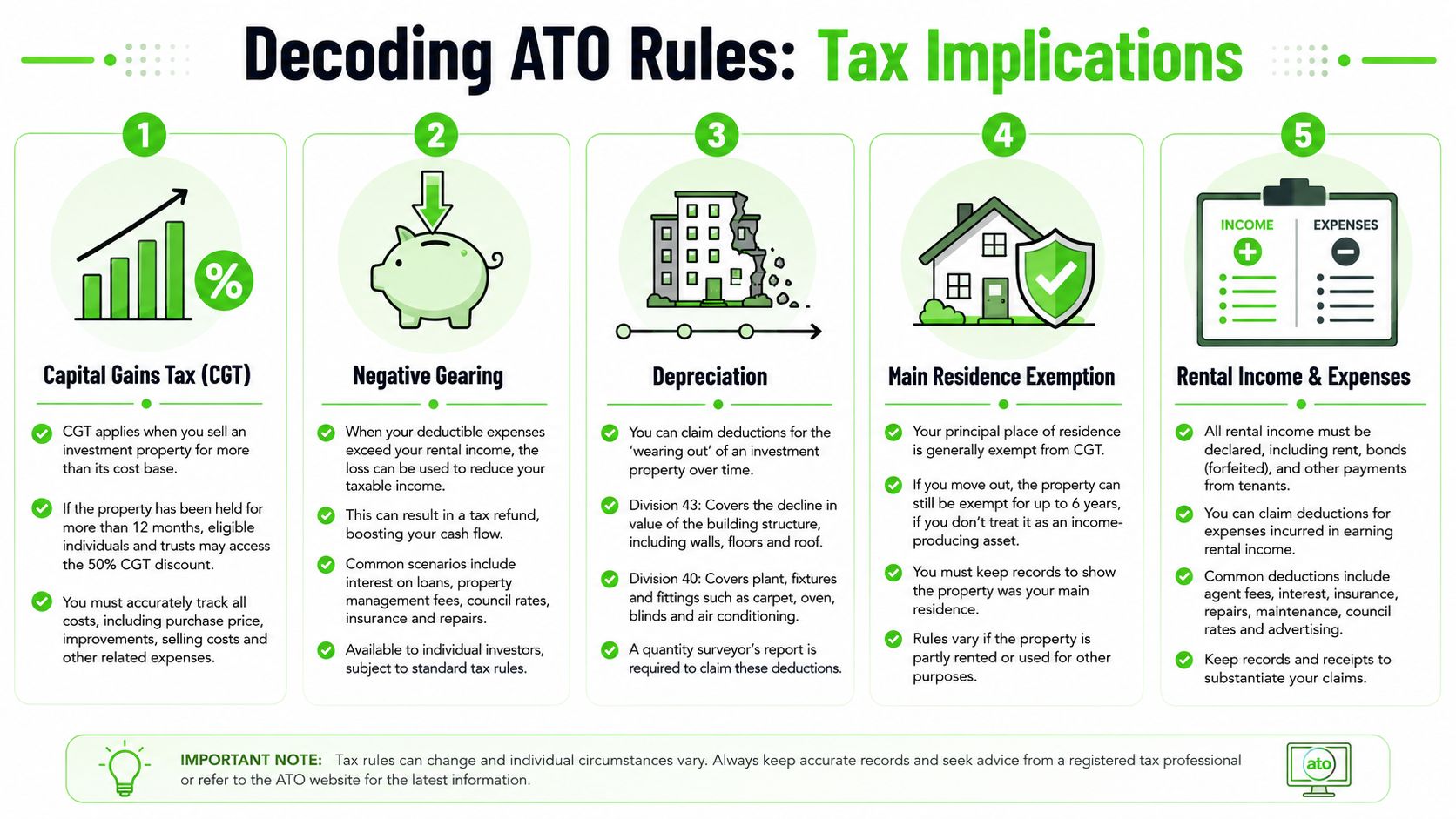

The Tax Implications A Deep Dive into ATO Rules

Tax usually settles the argument quickly.

A Sydney buyer looking at a Parramatta unit as a long-term rental is playing by one ATO rulebook. A family buying a Byron Bay house for school holidays, then listing it on Airbnb for part of the year, is dealing with a different one. That distinction affects what you can deduct each year, how you apportion costs, and what happens when you sell.

Negative gearing only works when the property is income producing on ATO terms

For a straightforward investment property, the tax treatment is familiar. If the property is rented, or clearly held out for rent, owners may be able to claim expenses such as interest, council rates, agent fees, insurance, eligible repairs, and depreciation. If those costs exceed rental income, the loss may be used against other assessable income under Australia's negative gearing rules.

A second home does not get that treatment just because it earns some rent during the year.

This catches Byron Bay owners more than Sydney investors. A buyer may say, “we'll use it a few weeks and rent it out the rest of the time,” but the ATO looks at actual use, private access, and whether the property was available for rent at market rates. Private use means expenses usually need to be split. Inflated peak-season asking rents, blocked-out owner dates, or keeping the property available only on selective weekends can all weaken the deduction position.

If you want to identify rental property tax deductions properly, start with the boring records first: booking calendars, owner stays, invoices, management statements, and evidence that the property was available for rent.

Poor records are often the problem. Not the tax rule itself.

That is also why buyers should understand the tax treatment of conveyancing fees in Australia before exchange. Some purchase costs are not immediately deductible and instead form part of the property's cost base, which matters later for CGT.

CGT often changes the result more than the annual tax return

Many buyers focus on yearly deductions and miss the exit tax.

With an investment property, CGT is part of the return calculation from day one. If an individual holds the asset for more than 12 months, the 50% CGT discount may apply, but there can still be a sizeable taxable gain. In Sydney, where long-term capital growth often does more of the heavy lifting than rental yield, this matters a lot.

Second homes are where assumptions get expensive. Owners often treat a holiday house like an extension of their main residence, but that exemption does not automatically follow the property. Whether any main residence concession applies depends on how the property was used, whether another property was nominated as the main residence, and the timing of any change in use.

I regularly see buyers underestimate this in Byron Bay. They focus on the lifestyle value, hold the property for years, then get a shock when a partial or full CGT liability appears on sale because the home was never their main residence in the ATO sense.

Mixed-use properties need disciplined apportionment from day one

Mixed use is the category that causes the most trouble.

If you use the property privately for part of the year and rent it for the rest, the expense claim needs to reflect that split. You cannot treat the whole holding cost as deductible because the property earned some short-term rental income. Interest, rates, insurance, utilities, cleaning, and other expenses may all need to be apportioned based on actual rental use and private use.

That is the practical dividing line between a Sydney investment apartment and a Byron holiday house with occasional guest bookings. The Sydney asset is usually cleaner from a tax perspective. The Byron property often comes with more owner enjoyment, but also more record-keeping, more apportionment, and more room for error.

For most buyers, the tax position fits one of three buckets:

- Pure investment property. Bought for rent and capital growth. No planned personal use.

- Pure second home. Bought for lifestyle. Tax deductions are limited because private use drives the ownership story.

- Mixed-use property. Bought for both access and income. Apportionment, booking records, and CGT tracking need to be handled properly from the start.

Buyers do not need to memorise every ATO ruling. They do need to be honest about how they will use the property, because the tax treatment follows the facts.

This video gives a useful high-level overview before you speak to your accountant.

Financing and Lender Criteria

A bank will assess a Sydney investment unit and a Byron Bay weekender through very different credit settings, even if the purchase price is similar. Buyers often focus on intent. Lenders focus on repayment risk, usable income, and what happens if the property does not perform as expected.

Why banks treat the two purchases differently

A second home is often assessed closer to an owner-occupied loan, provided the story is consistent. An investment property is usually treated as a higher-risk exposure because the lender expects rent to form part of the repayment case and knows vacancies, rate rises, and holding cost blowouts can put pressure on serviceability.

That usually affects three things straight away. Deposit expectations, interest rate pricing, and how much of the proposed rent the bank is willing to count. Banks do not usually take projected rent at face value. They shade it, then test your repayments at a higher assessment rate.

In Sydney, that matters because many buyers already have a large home loan and less spare borrowing power than they think. In Byron Bay, the issue is often different. A buyer may have strong equity, but the lender can be cautious if the plan relies on seasonal holiday income or a mixed personal-use arrangement.

Banks back PAYG income and consistent business income first. Rental income helps, but only after the lender applies its own discount and servicing rules.

What gets a second home application over the line

The cleaner second-home files usually look like this:

- Strong surplus income from salary or business income, without needing guest income to make the numbers work.

- A credible ownership story that matches the loan purpose, such as regular family use, not a lifestyle purchase dressed up as an investment.

- Available equity or cash for deposit, stamp duty, and a buffer for higher rates and ongoing costs.

- Low reliance on short-term letting income, especially in markets where occupancy can swing sharply across the year.

A Byron Bay buyer who says, "We will use it on school holidays and rent it out the rest of the time," may still get approved, but the structure becomes more complex if the servicing case depends on short-stay income. Some lenders are conservative on that point for good reason.

What strengthens an investment property application

For an investment purchase, lenders want a file that stands up under pressure.

- Rent assumptions grounded in local leasing evidence, not peak-holiday Airbnb screenshots. A proper rental market analysis for the target suburb carries more weight than optimistic online estimates.

- A stronger cash contribution, because higher-LVR investment lending can be more restricted and more expensive.

- A simple portfolio position, particularly if you already own multiple properties, carry personal debt, or have fluctuating self-employed income.

- Proof you can hold the asset through vacancy or rate changes, not just in a best-case month.

If you want a broad framework for assessing local rent conditions, Prophaven rental market insights offer a useful external reference point, but an Australian lender will still want local evidence that matches the suburb, dwelling type, and lease market you are buying into.

The practical mistake I see most often is buyers trying to finance a lifestyle property as if it were a standard investment. The lender can usually spot the mismatch. A beachfront apartment in Byron that will be blocked out for family use during peak periods does not present like a clean investment asset, even if it produces some income.

Approval is only part of the job. The better question is whether the loan structure matches the property's real use, your cash flow, and the ATO treatment you will be living with after settlement.

Cash Flow Scenarios Sydney vs Byron Bay

A buyer choosing between a Sydney investment unit and a Byron Bay holiday home is usually choosing between two very different holding costs.

The Sydney asset often asks for a manageable annual contribution in exchange for cleaner tax treatment, simpler management, and exposure to a deep metro market. The Byron property usually asks for more cash, more administration, and more discipline around private use. That does not make Byron a bad purchase. It means the numbers need to be judged as a lifestyle decision first, with income as secondary support.

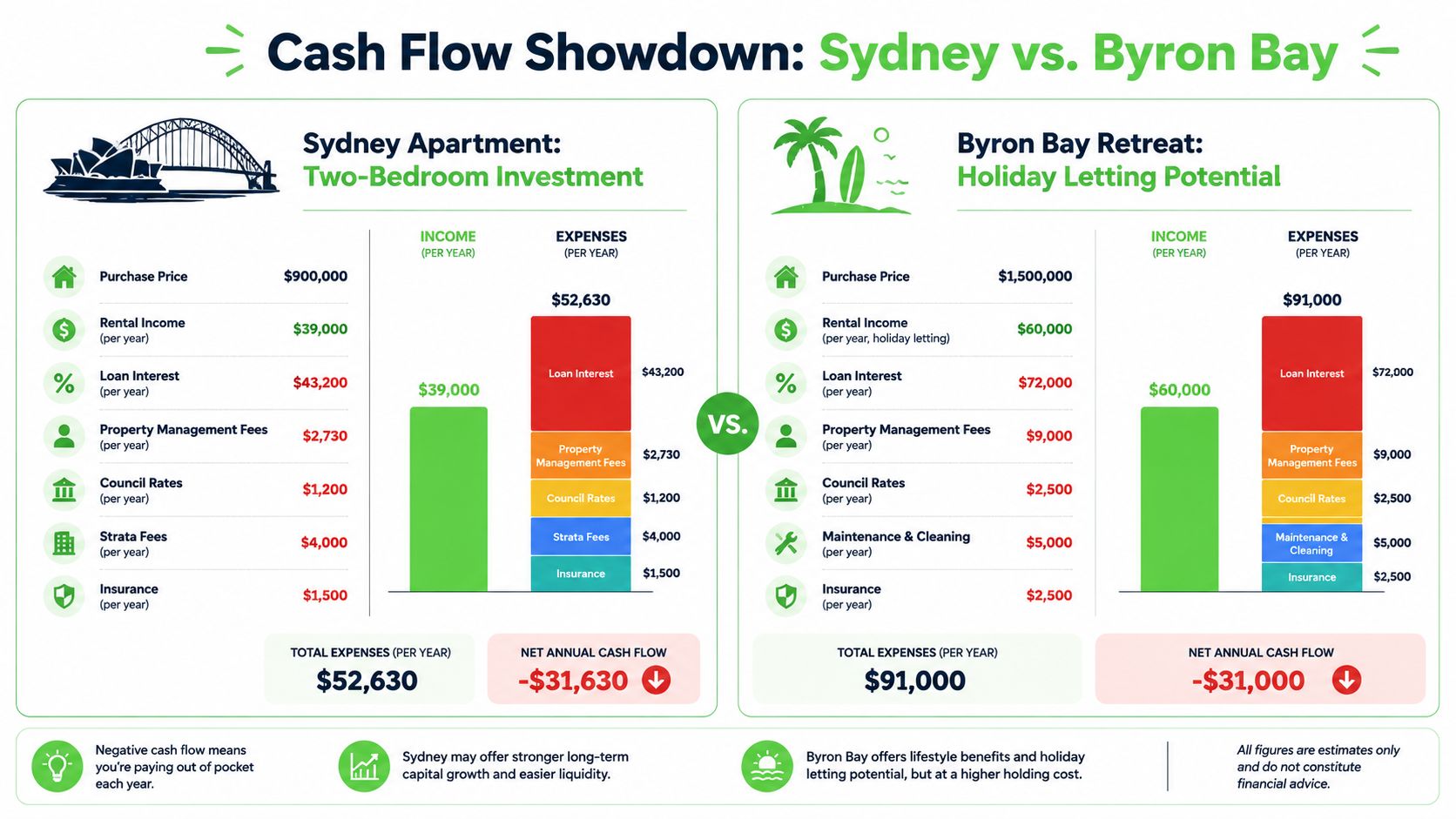

Scenario one Sydney apartment bought as an investment

Start with a $900,000 two-bedroom apartment in Sydney.

Using the figures provided for this scenario, the annual rent is $39,000, loan interest is $43,200, property management is $2,730, council rates are $1,200, strata is $4,000, insurance is $1,500, total expenses are $52,630, and the net annual cash flow is -$13,630.

That shortfall is familiar to Sydney investors. On a cash basis, the property is negatively geared before repairs, leasing fees, or vacancy are added. Even so, the model is straightforward. The property is held to produce rent, claim eligible deductions under ATO rules, and benefit from long-term capital growth in a market with broad owner-occupier and tenant demand.

In practice, this works best where the suburb has consistent leasing depth and the buyer can comfortably fund the annual gap without relying on tax refunds to rescue the deal. A proper suburb-level rental market analysis helps test that before you buy.

For a general framework on what drives rent performance, Prophaven rental market insights are a useful external reference. The local version matters more. In Sydney, a two-bed unit in Parramatta, Randwick, or Lane Cove can have very different vacancy risk, tenant profile, and rent resilience even at a similar price point.

Scenario two Byron Bay home used privately and rented part time

Now look at a $1,500,000 Byron Bay house.

Using the figures provided for this scenario, annual holiday-letting income is $60,000, loan interest is $72,000, property management is $9,000, council rates are $2,500, maintenance and cleaning are $5,000, insurance is $2,500, total expenses are $91,000, and the net annual cash flow is -$31,000.

That is a much heavier carry, and it is common in coastal lifestyle markets.

The headline income can look attractive, but Byron ownership costs build quickly. Short-stay management fees are higher. Cleaning and linen turnover are ongoing. Furnishing standards matter. Guest damage, empty gaps between bookings, and weather-related maintenance are more common than many buyers allow for in the first spreadsheet.

Private use changes the economics again. If you reserve school holidays, Easter, or summer for yourself, you are removing the strongest revenue periods from the letting calendar. As noted earlier, ATO treatment for mixed-use holiday homes also means expense claims are typically apportioned between income-producing use and private use. That is a real difference from a standard Sydney investment unit leased to a long-term tenant for the full year.

I tell clients to treat a Byron second home as a property that may offset part of its running cost, not as a pure yield play.

That framing avoids disappointment.

What these two examples tell you

The Sydney apartment is easier to assess because the purpose is clear. Rent is central to the strategy. Holding costs are easier to forecast. Management is usually lighter, especially with a stable long-term tenant and a competent local agent.

The Byron house can still be the right buy. For some households, having a family base in Byron is worth the larger annual shortfall, the higher maintenance load, and the more limited tax deductions that come with private use. The mistake is expecting it to behave like a metro investment property when it is really a lifestyle asset with some income attached.

Use this comparison as a quick filter:

| Question | Sydney investment apartment | Byron second home |

|---|---|---|

| Why are you buying it? | To build wealth through rent and growth | To use it and enjoy it |

| Can you justify it without tax help? | Often yes, if strategy is long-term | You should be able to |

| Is management simple? | Usually simpler with a long-term tenant | No, holiday letting is operationally heavy |

| Does private use complicate tax claims? | Usually no | Yes, often significantly |

If the property needs constant bookings, perfect weather, and generous tax assumptions to work, it is too tight. If your household can carry the cost comfortably and the purpose is clear, both models can work. They just serve different jobs.

Lifestyle Strategy and Ownership Rules

A spreadsheet won't tell you how annoying a property is to own.

Usage rules matter more in Byron than buyers expect

A Sydney investment leased to a long-term tenant is usually straightforward. You appoint a managing agent, approve maintenance, review rent, and hold the asset.

A Byron property is rarely that passive. If you want short-term letting flexibility, you need to think about local council settings, compliance, neighbour impact, and whether the property sits in a building or area with rules that limit your options. In apartments, strata by-laws can be just as important as market demand. In coastal locations, they can completely change the ownership experience.

This is why the rentvesting conversation matters for some buyers. Instead of forcing one property to do everything, they keep living where suits them and buy where the numbers work. This piece on rentvesting vs buying where you live is useful if you're torn between lifestyle location and investment discipline.

Structures insurance and management need to match the real use case

Ownership structure should follow purpose.

For an investment property, buyers commonly consider individual ownership, trusts, and in some cases more specialised structures depending on tax advice and long-term planning. For a second home intended for your family's use, those same structures may be less suitable or less efficient. The legal owner, the borrowing setup, and the intended use should all line up before you exchange contracts.

Then there's insurance.

- Landlord insurance suits a standard rental better than a holiday home with guest turnover.

- Holiday-home cover needs to reflect short stays, furnishings, public liability exposure, and vacant periods.

- Maintenance planning is heavier in coastal markets because salt air, storms, moisture, and guest use all accelerate wear.

A pure investment asks for discipline. A second home asks for tolerance. If you buy in Byron, you're not just buying a title. You're buying distance, weather exposure, guest expectations, and a second layer of life admin.

Making Your Final Decision A Checklist

Most buyers already know the answer before they ask the question. They just haven't framed it properly.

Use this checklist:

- Primary goal. Do you want wealth creation, or do you want a place your family will use?

- Cash flow tolerance. Can you comfortably carry the asset if rental income disappoints?

- Tax dependence. Does the purchase still make sense if deductions are less generous than you hoped?

- Management appetite. Are you willing to deal with tenants, guests, agents, maintenance, and compliance?

- Exit plan. Will you likely sell for portfolio reasons, keep it long term, or convert its use later?

- Lifestyle reality. Will you use the second home enough to justify tying up capital in it?

- Professional advice. Have your accountant and broker reviewed the intended use before you commit?

If your answer is mostly about return, flexibility, and cleaner tax treatment, an investment property is usually the better choice.

If your answer is mostly about weekends, family use, and long-term enjoyment, a second home can still be the right move. Just don't dress it up as an investment if the numbers only work on paper.

If you're weighing Sydney investment options against a Byron Bay lifestyle purchase, We Are Buyers Agents can help you test the strategy before you commit to the property. The right decision usually becomes clear once the numbers, tax position, lending path, and real-world ownership burden are looked at together.