You're probably seeing the same thing most investors are seeing right now. One headline says rates will crush borrowing power. Another says premium suburbs are still holding up. A podcast tells you to chase cash flow. A friend tells you Sydney property is impossible unless you're already wealthy. Then Byron Bay enters the conversation and the whole thing gets even murkier because lifestyle demand, local rules, and holiday letting can distort what looks like a straightforward investment.

That confusion is normal. The problem isn't a lack of information. It's that most advice for property investors stays generic long after the market has become more demanding.

A workable investment plan in Australia now has to handle tighter finance, higher holding costs, more experienced competition, and suburb-by-suburb differences that matter far more than broad national commentary. If you're buying in places like Sydney or Byron Bay, the margin for error is slimmer. A pretty property can still be a poor investment. A lower-yield asset can still be a smart buy. The skill is knowing which is which before you commit.

Table of Contents

- Navigating the 2026 Australian Property Market

- Shifting from Speculation to Strategy

- Structuring Your Finances for Success

- Your Blueprint for Bulletproof Due Diligence

- Finding Opportunity in Sydney and Byron Bay

- Why Smart Investors Use a Buyer's Agent

- Growing Your Portfolio After the Purchase

Navigating the 2026 Australian Property Market

The Australian investor who does well in this environment usually isn't the one with the hottest take. It's the one with the cleaner process.

That matters because the market is asking tougher questions than it did in easier credit conditions. Can the property carry itself if rates stay high for longer? Can you absorb repairs without forcing a sale? Are you buying for income, growth, flexibility, or a mix of all three? If you don't answer those before you buy, the market answers them for you later.

Sydney and Byron Bay make that even more obvious. Sydney gives you depth, infrastructure, and a wide spread between blue-chip, middle-ring, and emerging pockets. Byron Bay gives you scarcity, lifestyle demand, and a very different regulatory and management reality. The same investor can make a smart purchase in either market, but not with the same assumptions.

What buyers need to stop doing

A lot of first-time investors still make decisions in this order:

- They pick a suburb because it feels familiar.

- They find a property that looks safe.

- They ask the broker if the numbers can work.

- They hope growth fixes the weak spots.

That order is backwards. A resilient purchase starts with borrowing capacity, holding capacity, target outcome, and risk tolerance. The property comes later.

Buy the asset that fits your plan, not the asset that flatters your ego.

What practical advice looks like now

Useful advice for property investors should help you decide things such as:

- Whether a low-yield premium asset still fits if your income is strong and your time horizon is long.

- Whether to prefer a unit over a house when the entry price, strata position, and tenant demand make the unit the cleaner investment.

- Whether to buy remotely when local supply is tight but the opportunity is in another city or region.

- Whether to sit out a deal because the downside is obvious once you stop relying on optimistic assumptions.

Good investing isn't about always buying. It's about buying well, with enough margin in the numbers and enough discipline in the structure to stay in the game.

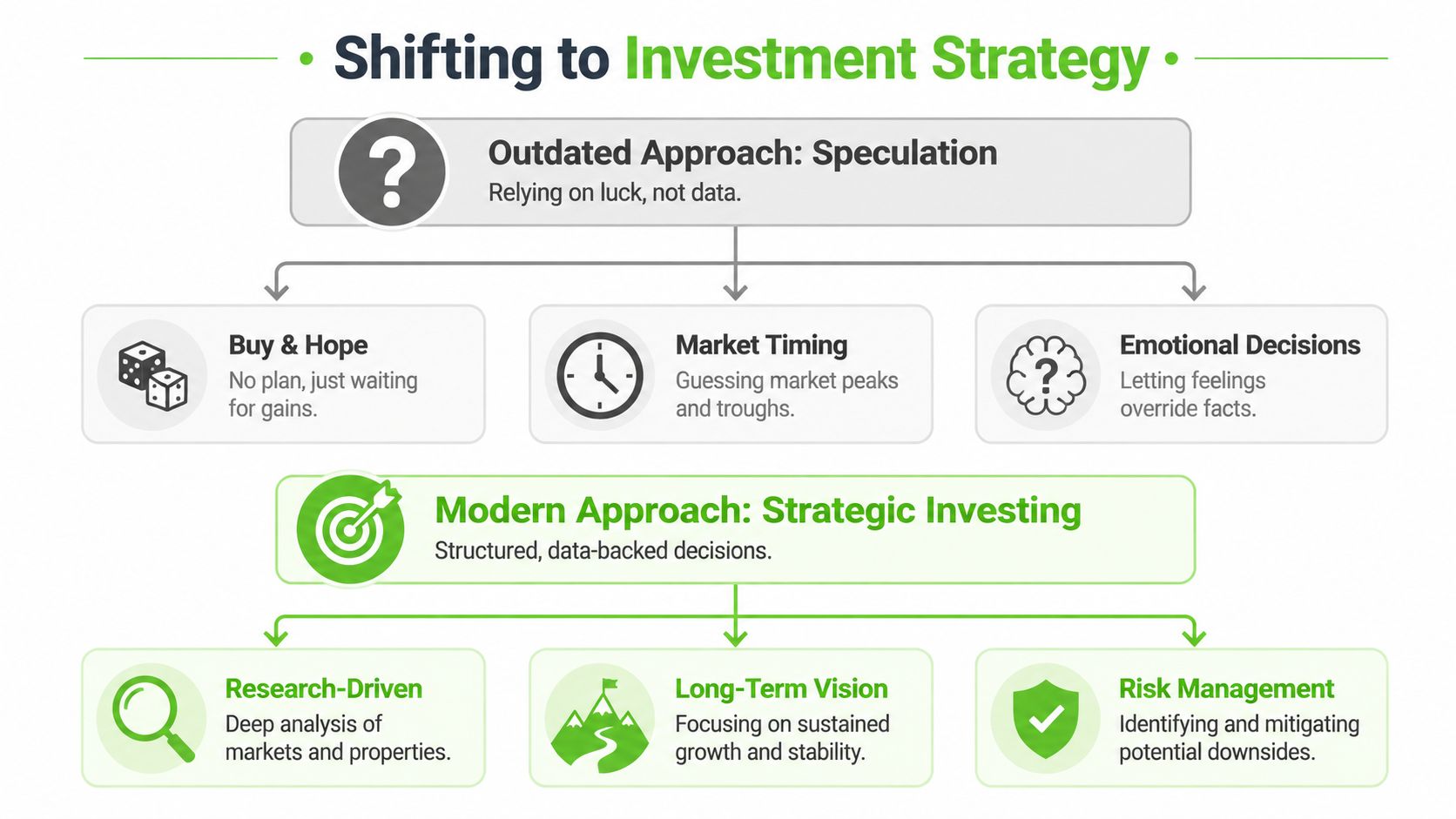

Shifting from Speculation to Strategy

The old model was simple. Buy something decent, wait, and assume the market would do the heavy lifting.

That approach still tempts people because it sounds easy. In practice, it leaves investors exposed to weak cash flow, poor asset selection, and rushed decisions made under auction pressure or fear of missing out. Property is no longer a space where amateurs casually compete with only owner-occupiers.

Why the old playbook struggles now

In the U.S. single-family rental market, the share of sales involving rental properties owned by non-individual investors rose from 18% in 2001 to 27% in 2021, according to the Joint Center for Housing Studies of Harvard University. The same source notes that institutional investors held roughly 574,000 single-family homes as of June 2022. The specific figures are U.S.-based, but the practical lesson travels well. Buyers are often up against professional capital that underwrites quickly and treats property like a business.

That's why strategic investors work from a framework, not a mood.

There's a useful parallel in other capital-heavy decisions. Businesses that review long-term operating costs before committing to equipment tend to make better calls than businesses that buy on sticker price alone. The same logic shows up in guides on how Australian businesses adopt renewables. Serious buyers model the lifetime economics before they sign. Property investors should do the same.

The three decisions that shape every purchase

A sound strategy usually rests on three decisions.

Goals first

Some buyers want borrowing-friendly assets with stable rent. Others will accept thinner income today because they want land content, scarcity, and a stronger long-term growth profile. Others again are rentvesting, renting where they want to live while buying where the numbers work better.

Write the goal in plain English. “I want an asset that I can hold comfortably through a tougher lending cycle” is clearer than “I want a good investment.”

Know your risk tolerance

Risk tolerance in property isn't abstract. It shows up in very ordinary moments. Can you carry a vacancy without stress? Can you handle a major repair and still sleep at night? Would a slower-growth but simpler asset keep you more disciplined than a glamour suburb purchase with tighter cash flow?

If the answer is no, the strategy needs adjusting.

Choose a model that fits your life

Different investors need different models:

| Investment model | Usually suits | Main trade-off |

|---|---|---|

| High-growth, lower-yield asset | Higher-income borrowers with longer horizons | Tighter holding costs |

| Balanced asset | Buyers who want some income and some upside | Less dramatic on either front |

| Rentvesting approach | Owner-occupiers priced out of preferred suburbs | Requires emotional discipline |

Practical rule: Strategy should make your next ten years easier to manage, not harder to justify.

The strongest advice for property investors is often the least exciting. Set the rules before you inspect a property. If you build the framework first, you'll reject more stock, but the purchases you do make are usually far stronger.

Structuring Your Finances for Success

Finance isn't just about getting approved. It's about building a structure that gives you room to operate after settlement.

That distinction matters most in expensive markets. A buyer who stretches to secure a property but leaves no buffer has not solved the problem. They've delayed it. The investors who stay active over time usually protect serviceability, liquidity, and flexibility before they chase an extra bit of borrowing capacity.

Finance structure matters as much as price

Pre-approval matters because speed matters. In competitive parts of Sydney, and in tightly held lifestyle markets, hesitation can cost you the deal. More importantly, pre-approval forces a hard look at what the bank may support and what your own budget should support. Those are not always the same number.

Loan structure also affects resilience. Interest-only can help preserve cash flow during a hold period. Principal and interest can reduce debt more steadily. An offset account can improve flexibility if you want to keep accessible cash while reducing interest exposure. None of these tools is automatically right. They're useful when they suit the investor's strategy, tax position, and tolerance for risk.

A good broker helps with product selection. A good investor still checks whether the structure fits the plan.

Use quick filters before deep analysis

Rules of thumb are useful when you treat them as filters, not as gospel. Investopedia's overview of real estate investing notes the 2% rule, which says a property looks attractive if monthly rent is at least 2% of the purchase price. The same source explains the 55% rule, which assumes around 45% of gross rent is consumed by vacancy, insurance, maintenance, taxes, and management, leaving about 55% as a rough proxy for net operating income. For broader context, it also notes that a 6% to 8% cap rate is generally considered good, while 3% to 4% is weak, in that framework of analysis from Investopedia's real estate investing guide.

Those numbers are screening tools. They are not a substitute for local underwriting.

In premium Australian markets, many assets won't meet a simple rule of thumb and may still be worth considering. Sydney is the obvious example. A quality asset in a strong school catchment, close to transport and employment, may fail a quick yield screen but still suit a buyer with stable income and a long holding period. That doesn't make the rule useless. It just means you use it to identify what you're giving up.

How investors stay conservative without freezing up

Here's a more useful way to think about finance in a high-cost market:

- Start with holding power: If the property is vacant, you still need to be comfortable.

- Model actual expenses: Include council rates, insurance, management, maintenance, strata if relevant, and realistic vacancy.

- Keep buffers accessible: An offset account often matters more in practice than squeezing every available dollar into the purchase.

- Don't rely on tax to rescue a weak deal: Tax outcomes can help, but they shouldn't be the reason the deal works.

For investors trying to understand how deductions and negative gearing fit into the broader picture, a practical summary of tax benefits for property investors can help frame the discussion before you sit down with your accountant.

The cleanest deal is the one that still looks acceptable after you remove the optimistic assumptions.

In real terms, that means being willing to buy below your theoretical maximum. It's not flashy, but it keeps options open when lending settings, rent conditions, or household expenses change.

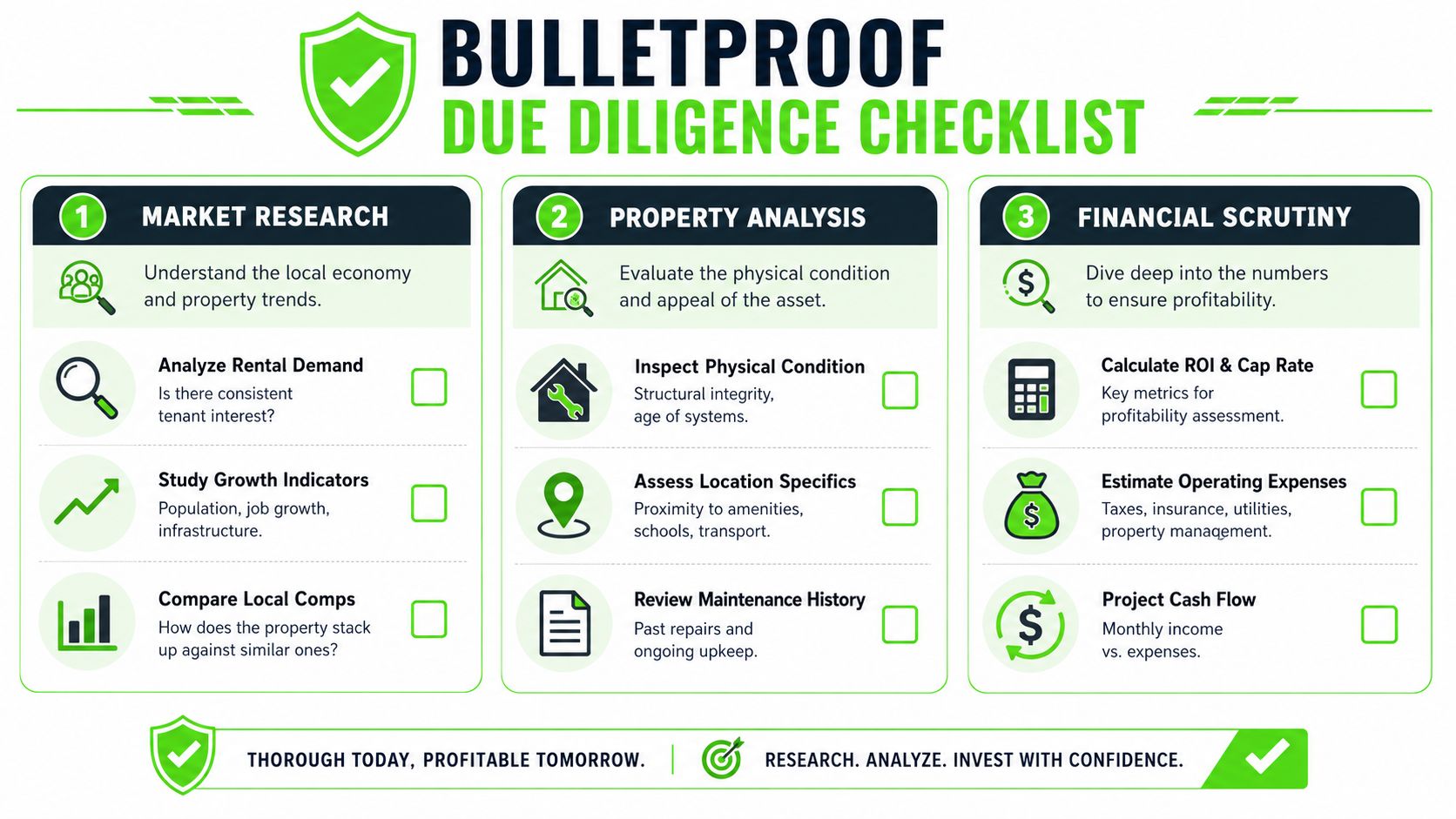

Your Blueprint for Bulletproof Due Diligence

Due diligence is where many investors either protect themselves or talk themselves into trouble.

The phrase gets used so often that it becomes meaningless. In practice, proper due diligence is a sequence. First you test the market. Then you test the property. Then you test the numbers again with the actual facts you've uncovered. If any layer fails, you reassess or walk.

Market checks before property checks

Start at suburb level before you get attached to a specific address. Look at current supply, tenant appeal, transport links, school catchments, local planning changes, and the type of stock being added. In Sydney, that may mean checking whether a pocket is seeing a large wave of new apartments that could compete on rent. In Byron Bay, it may mean understanding how local regulation affects use, occupancy, and management complexity.

A simple way to organise the work is to adapt a structured property review list such as Homebase's due diligence checklist, then customise it for Australian conditions, council rules, and your own investment criteria.

Useful market due diligence often includes:

- Comparable rentals: Check what similar stock is leasing for, not what hopeful listings advertise.

- Buyer depth: Some properties resell easily. Some only appeal to a narrow slice of the market.

- Council and zoning context: Future development can help value or hurt amenity.

- Street-level reality: Main roads, flood exposure, noise, poor access, and awkward topography all matter.

What to verify on the asset itself

Once the market makes sense, move to the property.

For houses, building and pest checks are standard. For apartments, the strata side can be just as important as the physical inspection. A tidy unit in a troubled building is not a tidy investment. Meeting minutes, levies, maintenance history, upcoming works, by-laws, and defect discussions all need attention. If you're buying a house or townhouse, the practical points covered in this guide to building and pest inspection are worth folding into your checklist.

I'd break asset-level due diligence into three questions:

| Question | What you're testing | Why it matters |

|---|---|---|

| Is it sound? | Structure, moisture, pests, services, defects | Surprise costs hurt holding power |

| Is it rentable? | Layout, natural light, parking, storage, privacy | Tenant demand is practical, not theoretical |

| Is it saleable later? | Floor plan, position, building quality, street appeal | Exit matters before entry |

Ignore cosmetic presentation during due diligence. Tenants and future buyers live with layout, noise, defects, and access long after styling disappears.

A remote buying playbook that reduces risk

Remote buying is no longer unusual, but generic advice rarely gets specific enough. Guidance on sight-unseen investing consistently points to live remote walk-throughs, independent inspection reports, and experienced local professionals as the core safeguards, as outlined in this article on buying property sight-unseen.

That only works if you treat verification as a system.

Use a layered process:

- Get a live video walk-through rather than relying only on polished marketing footage.

- Ask the person on site to pause on problem areas such as ceilings, external walls, wet areas, boundaries, and views from each window.

- Order independent reports rather than accepting verbal reassurance.

- Cross-check the rent estimate with actual competing listings and local managers.

- Use a local buyer's agent or trusted representative if the market moves fast and inspections are hard to coordinate.

Remote buying can work very well. Sloppy remote buying is where people overpay, miss defects, or misunderstand the location.

Finding Opportunity in Sydney and Byron Bay

Sydney and Byron Bay are both attractive markets. They are not interchangeable investment environments.

Sydney gives you a broad economy, deep tenant pools, and many micro-markets inside one city. Byron Bay gives you scarcity, lifestyle appeal, and a market where local knowledge can matter more than broad state-level commentary. Investors who treat them the same usually misprice the risk.

Sydney requires precision not blind optimism

Sydney often forces a sharper choice between yield and quality. Many buyers won't get both. That means you need to know what you're deliberately sacrificing.

A lower-yield asset can make sense in Sydney if the location has durable owner-occupier appeal, strong transport access, good schools, and a buyer pool that remains broad in softer conditions. In some cases, a well-located apartment can be the better investment than a compromised house on a busy road or in a patchy pocket. The right unit in the right block often beats the wrong house bought because “land always wins.”

The work here is local. You need to know which suburbs are being reshaped by infrastructure, which pockets remain tenant-friendly at the current entry point, and which buildings carry hidden strata or defect risk. A suburb-level rental market analysis is often more useful than another national forecast.

Byron Bay rewards local knowledge and punishes shortcuts

Byron Bay is different. Buyers are often drawn in by scarcity and lifestyle appeal, then underestimate the operating reality.

The headline rent or holiday potential can look attractive, but the practical issues sit underneath that. Management intensity, seasonality, local rules, neighbour sensitivity, maintenance exposure, and the gap between peak demand and ordinary periods all matter. Some investors suit Byron well because they understand they're buying a tightly held lifestyle market with operational complexity. Others would be better served by a simpler long-term rental in a less glamorous location.

That's where generic “buy for cash flow” advice breaks down.

How to decide between growth and cash flow

In a higher-cost environment, investors need to question whether prioritising cash flow over capital growth still holds in every case. Borrowing, insurance, and compliance costs can change the answer. What matters is stress-testing the investment against rate rises, vacancy, and repair shocks, which is the core argument in this discussion of common pitfalls of real estate investing.

A practical comparison looks like this:

- Sydney growth play: You may accept a lower initial yield because the asset is scarce, well located, and easy to hold from an income perspective.

- Byron lifestyle-investment play: You need to be much stricter on operating assumptions because gross income can flatter the true net result.

- Balanced approach: Some investors blend a premium-market purchase with a more straightforward income-producing asset elsewhere.

Good investors don't ask, “Which market is better?” They ask, “Which market fits my balance sheet, risk tolerance, and holding capacity?”

If you need the property to support itself comfortably from day one, some Sydney and Byron stock will fail that test. If your priority is long-term asset quality and you can hold confidently, the right premium-market purchase can still be sensible. The key is that the decision is conscious, not accidental.

Why Smart Investors Use a Buyer's Agent

Most investors don't need more listings. They need better judgement at the point of decision.

That's where a buyer's agent can earn their place. A selling agent works for the vendor. A buyer's agent represents the buyer's brief, negotiates from the buyer's side, and helps filter, assess, and execute against a strategy. In a busy market, that difference is practical, not semantic.

What the right adviser actually does

A good buyer's agent does far more than open doors.

They can help narrow the buy brief, pressure-test suburb selection, assess a property against comparable evidence, coordinate due diligence, and handle negotiation with less emotion than most buyers bring to the process. They may also provide access to opportunities that never become broad online campaigns.

That matters even more if you're buying in a location you don't know street by street, or if you're trying to invest while managing a full-time job and family life. One factual example in this space is buyers agent services in Australia, which outlines the role as research, search, evaluation, and negotiation support for purchasers rather than vendors.

A short explanation often helps more than a long one. This video gives a practical look at how the process works in real buying situations.

When the fee makes sense

The fee makes sense when the agent changes the outcome. That could mean stopping you from buying a poor asset. It could mean negotiating more effectively. It could mean identifying a better-fit property that you wouldn't have found or correctly assessed on your own.

It won't suit every buyer. If you have the time, local knowledge, valuation skill, and negotiation discipline, you may choose to do it yourself. But many investors underestimate the cost of mistakes. Overpaying, buying the wrong stock, missing a defect pattern, or choosing the wrong block can drag on returns for years.

The right adviser doesn't remove risk. They help you see it earlier, price it properly, and avoid paying premium money for average property.

That's usually the true value. Not convenience alone. Better decisions under pressure.

Growing Your Portfolio After the Purchase

Settlement isn't the finish line. It's where portfolio management starts.

A property can be bought well and still underperform if the ownership phase is handled lazily. Rent reviews get missed. Maintenance gets deferred until it becomes expensive. Insurance sits untouched. A mediocre property manager lets tenant quality slip. Investors who think carefully before purchase but go passive after settlement often leave a lot on the table.

Ownership is where results are made

Good post-purchase management is usually unglamorous.

Choose a property manager who communicates clearly, understands the local tenant pool, and acts early on arrears, maintenance, and lease renewal timing. Review rents regularly against live competing stock, not against what the property rented for last year. Keep a separate maintenance reserve so ordinary repairs don't derail your monthly cash position.

Three habits make a big difference:

- Review income regularly: Don't let the rent drift behind the market without good reason.

- Stay ahead on maintenance: Small defects become large ones when ignored.

- Track actual performance: Compare the actual result against the assumptions you used when buying.

Review the portfolio not just the property

As equity builds, the smarter question becomes whether each asset is still doing the job you bought it to do.

One property may be your long-term cornerstone because the location and asset quality remain strong. Another may no longer fit your strategy because the management burden is too high, the building issues are mounting, or the capital is better deployed elsewhere. Portfolio growth is often less about buying more and more about reviewing with honesty.

That review should ask:

| Portfolio question | Why it matters |

|---|---|

| Is this asset still aligned with the original strategy? | Markets and personal circumstances change |

| Is the property easy to hold? | Holding power protects long-term outcomes |

| Would I buy this asset again today? | If not, work out why |

| Is accrued equity best used here or elsewhere? | Growth comes from allocation, not just accumulation |

Property investing rewards patience, but not passivity. The investors who last are the ones who buy with discipline, hold with structure, and make their next move from evidence rather than noise.

If you want clear, location-specific advice for property investors in Sydney, Byron Bay, or other Australian markets, speak with the team at We Are Buyers Agents. A good brief, clean numbers, and disciplined due diligence can save years of expensive trial and error.