You've probably had this thought already. Your investment property has risen in value, your loan statements still look heavier than they should, and a decent chunk of equity is sitting there doing nothing. At the same time, rates, lender policy, and your next purchase plans have all changed since you first took the loan out.

That's where an investment property refinance stops being a paperwork exercise and becomes a portfolio decision. The right refinance can improve cash flow, release equity for the next deposit, tidy up poor debt structure, or give you features that help you manage money properly. The wrong refinance can lock you into the wrong lender, dilute tax deductibility, or leave you with a bigger loan that doesn't materially improve your position.

I look at refinance strategy the same way I look at acquisitions. Start with the objective. Then test whether the numbers, lending policy, and timing support it.

Table of Contents

- Is Now the Right Time to Refinance Your Investment

- Crunching the Numbers on Your Refinance

- Preparing Your Refinance Application for Success

- How to Compare Australian Lenders and Loan Products

- Understanding the Tax and Legal Implications

- Strategic Timing Risks and When to Call a Professional

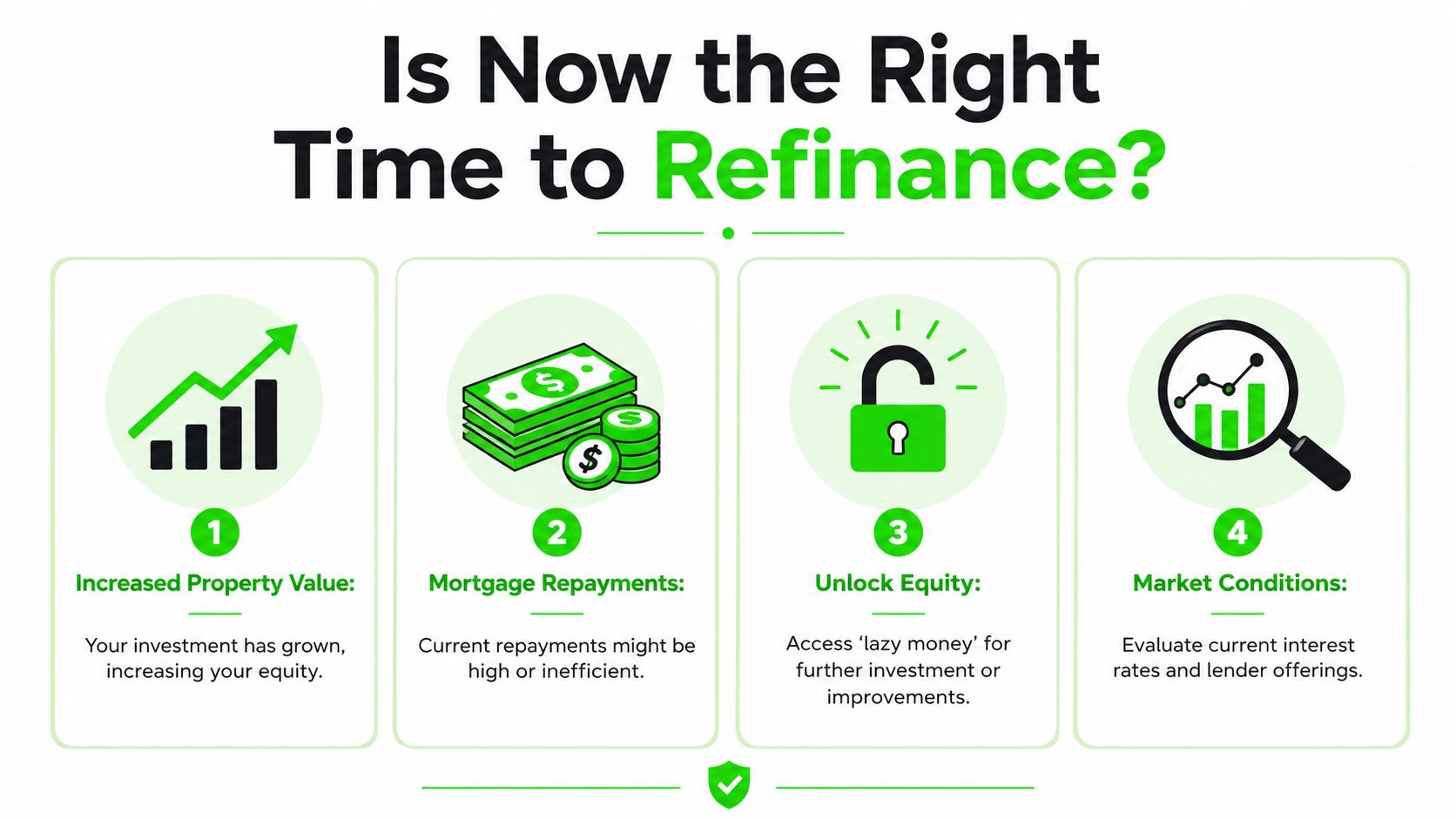

Is Now the Right Time to Refinance Your Investment

A lot of investors assume refinancing is only worth doing when there's a sharply lower rate on offer. That's too narrow. In practice, the better question is whether your current loan still fits the job your portfolio needs it to do.

According to the Australian Bureau of Statistics, refinancing activity for investment loans in Australia was 18.7% higher in the September 2025 quarter than the same period a year earlier, while investors accounted for around 40% of all new mortgages in a $12 trillion residential market, as reported in this Australian property lending update. That tells you something important. Investors aren't just chasing a slightly cheaper repayment. They're actively restructuring debt.

Why investors are refinancing now

Most borrowers sit in one of two camps. Either they've held the property long enough to build equity and want that equity working, or they're carrying a loan structure that made sense years ago but now limits cash flow and borrowing capacity.

If your property has performed well, your equity may be “lazy” in the sense that it exists on paper but isn't supporting your next move. If your interest rate is uncompetitive, your cash flow may be tighter than it needs to be. If you've got personal debt mixed into the wrong facility, your structure may be costing you flexibility and possibly tax efficiency.

Practical rule: Refinance because it improves your position, not because a lender advertises a sharp headline rate.

The four refinance goals that matter

There are four strategic reasons I see most often.

Improve cash flow

This is the simplest one. If you can reduce the interest burden or move to a better loan structure, the property may hold itself more comfortably. That matters when you're trying to keep serviceability intact for the next purchase.

Release equity for another acquisition

Refinance can be a growth tool. Equity can fund a deposit, costs, or renovations on the next asset. But only if the numbers stack up and the lender will let you access it on acceptable terms.

Consolidate debt

Sometimes an investor has scattered debts across credit cards, personal loans, or poorly structured splits. Rolling debt into a cleaner arrangement can simplify cash flow. It can also create tax complications if done badly, so the structure matters more than the marketing.

Upgrade the loan features

A good offset account, cleaner splits, or a more flexible product can be worth more than a tiny rate discount. Investors often underestimate how much damage a clunky loan does over time.

One more point. The right time to refinance isn't always when rates are moving. It's when your current debt structure no longer matches your strategy.

Sydney and Byron Bay investors often focus on the property first and the debt second. In reality, poor debt structure can slow portfolio growth just as much as buying the wrong asset.

Crunching the Numbers on Your Refinance

A refinance only makes sense if it improves your position in a measurable way. For an investor, that usually means one of three outcomes. Better cash flow, usable equity for the next purchase, or a cleaner debt structure that stops bad lending decisions from dragging on the portfolio.

Start there. A lower rate on its own is not enough.

Work out the real break-even point

I usually run this test before I discuss products. If the costs take too long to recover, the refinance is often a distraction, especially if you may sell, renovate, or buy again in the next year or two.

The basic calculation is simple.

| Metric | Value |

|---|---|

| Current loan repayment | Your existing monthly repayment |

| Proposed new repayment | The new monthly repayment |

| Monthly saving | Current repayment minus new repayment |

| Upfront refinance costs | Discharge fee, application fee, valuation, settlement costs, and any government charges |

| Break-even period | Upfront costs divided by monthly saving |

Here is what that looks like in practice. Say an investor has a $600,000 loan and can cut repayments by $280 a month, but the refinance costs $2,400 all up. The break-even point is about 8.5 months. That is reasonable if the loan also gives them an offset, better splits, or access to equity. If the saving is only $90 a month on the same costs, break-even blows out to more than two years. At that point, I would ask a harder question. What problem is this refinance actually solving?

That question matters because investors often focus on the rate and miss the structure. A loan that saves a small amount each month but traps future equity, mixes deductible and non-deductible debt, or limits cash-out can cost far more over the next acquisition cycle.

Monthly savings matter. Strategy matters more.

Calculate usable equity, not the headline equity number

Plenty of investors look at an updated property estimate and assume that full gain is available to borrow against. It rarely works that way.

In the Australian market, lenders commonly become much more conservative once an investment loan goes above 80% LVR, particularly if Lenders Mortgage Insurance enters the picture. Even below that point, accessible equity is only one part of the decision. Serviceability still has to stack up, and some lenders are far more generous than others on rental income shading, existing debts, and living expense treatment.

A clean starting formula is:

Usable equity = 80% of current property value minus current loan balance

For example, if a property is worth $900,000 and the current loan is $620,000, 80% of the value is $720,000. That leaves roughly $100,000 in usable equity before costs. In real life, I would trim that expectation further because valuation risk, refinance fees, and cash buffers matter.

Then comes the part many online guides skip. Should you release that equity?

If the goal is a new acquisition, released funds need to support a property that improves the portfolio, not just adds another debt. That is where buyers make expensive mistakes. They pull out equity because they can, then place it into a weak suburb, a poor yield asset, or a property with no clear role in the broader plan. Before using equity for the next purchase, get clear on the target area's supply, rents, vacancy pressure, and tenant demand. A proper rental market analysis for investment decision-making helps test whether the next property is likely to strengthen serviceability or strain it.

Compare the refinance against the alternatives

This is the strategic part. Refinancing is not always the best move, even when the numbers look acceptable.

A rate-and-term refinance may improve cash flow with minimal disruption. A cash-out refinance may help fund the next deposit, but it can also reduce buffers and tighten borrowing capacity if the lender loads the new debt heavily in serviceability. Debt consolidation can simplify repayments, but if investment and personal debt are blended carelessly, the tax treatment can become messy fast.

Non-bank lenders also need a proper look here. In Australia, they can be useful for investors with complex income, trust structures, recent credit issues, or servicing pressure with major banks. But the trade-off is usually a higher rate, different fee profile, or less generous features. Sometimes that is a smart short-term move to get a deal done and refinance again later. Sometimes it is an expensive patch that delays a permanent fix.

That is why I treat refinancing as a portfolio decision first and a loan process second. The best refinance is the one that gives you a clear advantage over the next two or three moves, not just the next repayment date.

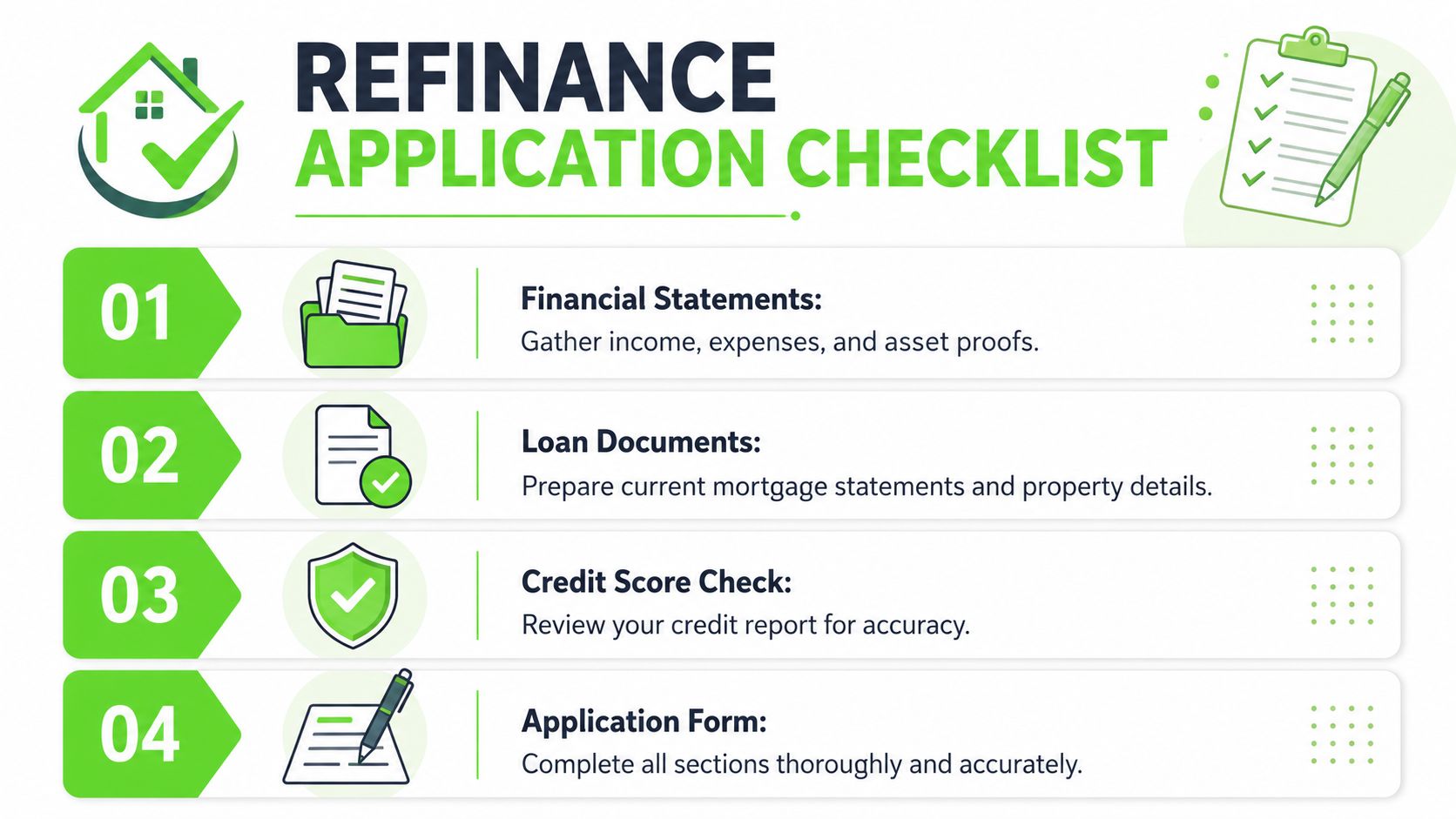

Preparing Your Refinance Application for Success

A refinance application succeeds or fails before credit ever looks at the rate. If the file does not clearly show why you are refinancing, where the equity is going, and how the new debt fits the rest of the portfolio, the lender starts filling gaps with caution.

That matters more for investors than owner-occupiers. A clean rate-and-term refinance is one thing. A cash-out refinance for the next deposit, a debt restructure across multiple properties, or a move to a non-bank lender because servicing is tight gets assessed much harder. I regularly see investors focus on the valuation and forget the story. Credit wants both.

Build the file around the purpose of the refinance

Start with the reason for the refinance, then gather documents that support it.

If the goal is to reduce repayments, show clean repayment history and stable income. If the goal is to release equity for another purchase, show where the funds are going and why the structure makes sense. If the goal is to consolidate debt, separate investment-purpose debt from personal debt properly so you do not create tax problems later.

For Australian investor loans, the document list usually includes:

- Income evidence. Payslips, tax returns, notices of assessment, and accountant-prepared financials if you are self-employed or buying in a trust.

- Rental income records. Current lease, managing agent statements, and evidence the rent being declared matches what is received.

- Debt statements. Existing home loans, investment loans, personal loans, credit cards, and buy now pay later accounts.

- Cash position. Savings statements, offset balances, and transaction accounts that support living expenses and conduct.

- Property documents. Council rates, insurance, current loan statements, and in some cases a recent lease renewal or tenancy ledger.

If you are restructuring cash flow, get the account setup right before you apply. Investors often ask whether redraw is enough. In practice, a proper offset usually gives cleaner control over cash and cleaner separation between personal and investment use. This guide on how an offset loan works for property investors explains the difference well.

What credit actually checks

Lenders test consistency first.

They compare the application form against bank statements, rental statements, tax returns, liabilities on your credit report, and the proposed purpose of the funds. If one part says the refinance is for investment, but the statements show unstable spending, recently opened consumer debt, or unexplained transfers, the file slows down. Sometimes it gets declined even when the equity position looks fine.

The practical issues are usually boring, but expensive:

- Messy account conduct. Dishonours, arrears, gambling transactions, or frequent overdrawn balances raise servicing and conduct concerns.

- Rental income that does not stack up. If the lease, agent statement, and declared rent do not match, the lender uses the lower figure or asks more questions.

- Missing liabilities. Undisclosed cards and personal loans damage credibility fast.

- Overconfidence on value. Online estimates do not decide the refinance. The lender's valuer does.

- Poor cash-out explanation. "Future investment" is often too vague. A clear use of funds gives credit less room to shade the risk up.

A good file reads cleanly. The assessor should be able to see your income, your debts, the property's performance, and the purpose of the refinance without guessing.

Watch the pressure points investors miss

LVR is one. Staying below the common threshold that avoids lenders mortgage insurance can preserve more of the benefit of the refinance, as noted earlier. But I would not stop there. The bigger risk is pulling out equity without leaving enough buffer for vacancy, rates, insurance, and repairs. On paper, a cash-out refinance can look sensible. In practice, a thin buffer turns one unexpected expense into a serviceability problem.

Investors renovating before refinance need to be even more careful. AmeriSave's BRRRR guide explains that many lenders apply seasoning rules before allowing cash-out against a higher post-renovation value, and it also points out how renovation overruns can hurt the refinance case. The Australian version of that problem is common. The works run over budget, the valuer comes in short, and the investor is left with expensive short-term debt or a half-finished plan.

That is one reason I often involve both broker and buyer's agent thinking before the application goes in. The broker works on policy fit, structure, and servicing. The buyer's agent pressure-tests whether the equity release is improving the portfolio or just creating more debt with no clear acquisition edge. If you are also looking outside Australia, the logic is similar. The lending structure needs to match the asset and jurisdiction, and finding financing for global properties gives a useful overview of that side of the decision.

The strongest refinance applications do one thing well. They make the lender comfortable that this is a deliberate portfolio move, not a scramble for cash.

How to Compare Australian Lenders and Loan Products

A refinance decision usually comes down to one question. Are you trying to lower holding costs, pull out usable equity for the next purchase, or clean up debt that is hurting serviceability?

Those goals point to different lenders.

The best lender depends on the job the refinance needs to do

I see investors lose time by comparing loans as if every refinance has the same purpose. They do not. A borrower chasing a sharper rate on a single investment property can often use a very different lender from a borrower trying to release equity for a Brisbane duplex purchase or roll expensive personal debt into a cleaner structure.

Start with the use case, then compare products against it.

If the goal is rate reduction, compare the full annual cost, not just the headline rate. A loan that is 0.20% cheaper can still be inferior once annual fees, package costs, and valuation fees are counted. On a $650,000 investment loan, that rate gap is meaningful, but it can be wiped out quickly by poor features or refinance costs if you are likely to restructure again within a year or two.

If the goal is cash-out for another acquisition, policy matters as much as price. Some lenders are comfortable with equity release for a clear investment purpose. Others become conservative once the portfolio grows, the security is unusual, or the borrower already carries several properties. The wrong lender can approve today's refinance and block the next purchase six months later.

If the goal is debt consolidation, be careful. Lowering repayments can improve monthly cash flow, but stretching short-term debt over a long property loan can increase total interest and muddy the tax position. That trade-off needs to be clear before you sign anything.

Compare four things, in this order

I usually assess lender options across four filters.

- Policy fit. Can the lender handle your income mix, rental treatment, property type, ownership structure, and intended cash-out purpose?

- Serviceability method. Two lenders can look similar on rate and produce very different borrowing capacities because they shade rent differently, treat existing debts differently, or take a harder line on living expenses.

- Product features. Investors often need split loans, interest-only options, and clean cash management. A proper offset account is often more practical than redraw if you want tighter control over investment funds. This guide on what an offset loan is explains the difference well.

- Total cost and flexibility. Compare the rate, annual fees, discharge costs, clawback risk, and how easy it will be to vary the structure later.

That order matters. There is no value in chasing a cheap rate from a lender whose policy does not fit your portfolio strategy.

Major banks, second-tier lenders, and non-banks all have a place

The major banks still suit many investors. They can be competitive on pricing, familiar to accountants and solicitors, and straightforward for vanilla scenarios.

Second-tier banks and non-bank lenders earn their place when the file stops looking vanilla. That includes investors with self-employed income, multiple entities, recent debt recycling, reliance on add-backs, or a portfolio that has grown faster than a mainstream credit team likes to see. In those cases, a non-bank lender is not a last resort. It can be the right first move if the policy matches the plan.

The trade-off is usually clear. You may pay a slightly higher rate or fee load in exchange for better borrowing capacity, a more workable cash-out policy, or a servicing model that leaves room for the next acquisition. For an investor buying again soon, that can be the smarter call than saving a few basis points today and getting boxed in later.

Portfolio size also changes the comparison. Some lenders become less attractive as property count rises, especially if you are stacking securities across several states or trust structures. Investors building beyond a small portfolio need to ask a harder question than "Who is cheapest?" The better question is "Who still works at property five, six, or seven?"

That is where a broker and buyer's agent can add real value together. The broker checks policy, servicing, and structure. The buyer's agent tests whether the released equity is being used for an asset that improves the portfolio, rather than just creating more debt.

If part of your investing plan is offshore, lender selection gets even narrower. The funding structure, security position, and borrower assessment can be very different. For broader context on finding financing for global properties, it helps to compare how overseas investment loans are assessed.

A short explainer can also help frame the product differences before you choose.

The best refinance loan is the one that supports the next move in your portfolio, not just the next repayment.

Understanding the Tax and Legal Implications

Refinancing changes more than your repayment. It can change the deductibility of costs, the cleanliness of your records, and the legal paperwork attached to the property.

Borrowing expenses and what you can claim

In Australia, the treatment of borrowing expenses is specific. Property Tax Specialists explains that if total borrowing expenses exceed $100, the deduction must be claimed over the loan term or five years, whichever is shorter. If the total is under $100, the full deduction is claimable in the income year incurred. The same source notes that if you repay the loan within five years, the remaining borrowing expenses may be claimed in the final year.

That's not a detail to gloss over. I still see investors assume all refinance costs are immediately deductible in one hit. Sometimes they are not.

If you want a broader checklist on investor tax habits that help maximize your tax deductions, it's worth reviewing one with your accountant before you settle the new loan.

The mixed purpose loan trap

Here, many otherwise sensible refinances go wrong.

If you refinance an investment property and release equity, the tax treatment depends on what that borrowed money is used for. If the funds go toward another investment purpose, the interest position may be very different from a situation where the money pays for private spending. That's why split structure matters. Keep investment use separate from personal use. Don't run everything through one blended facility and expect clean records later.

An investor choosing between an investment property and a lifestyle purchase should also understand that purpose changes tax outcomes. This comparison of investment property vs second home is a useful reminder that the same property debt doesn't always get treated the same way.

Legally, the refinance also requires discharge of the existing mortgage and registration of the new one. Your lender, broker, and conveyancer or solicitor usually manage that process, but errors in names, title details, or ownership structure can delay settlement. If the property is held in a trust, company, or changing ownership arrangement, get legal advice before documents are issued.

Keep loan purpose clean from day one. Fixing a contaminated structure later is usually harder than setting it up properly at refinance.

Strategic Timing Risks and When to Call a Professional

A refinance can be well-intentioned and still be badly timed. The risk usually isn't the idea itself. It's the gap between what the investor assumes will happen and what the lender, valuer, or market does.

The risks that derail a good refinance

The first risk is valuation. If the valuer comes in below your expectation, your equity release plan may shrink or disappear. That can knock out your next purchase before you've even started.

The second is cost drag. A loan that looks better on rate may still be poor value if break costs, fees, or restrictive features outweigh the practical benefit. Fixed-rate exits are where people get caught most often.

The third is debt utilization risk. Releasing equity feels productive, but more debt only helps if the new capital is deployed into a sound purchase with strong fundamentals. If you refinance just because you can, you may end up stretching cash flow without improving your portfolio.

Where a broker and buyer's agent add value

A capable mortgage broker earns their keep by matching strategy to lender policy. They know which lenders are investor-friendly, which ones handle cash-out cleanly, and which products look good in an ad but fail under servicing or policy.

A buyer's agent comes in on the deployment side. If you've pulled equity out, the next step matters more than the refinance itself. The whole exercise only works if the released funds go into an asset that fits your risk tolerance, borrowing profile, and long-term plan.

The cleanest outcomes usually happen when debt strategy and acquisition strategy are coordinated. Refinance first, structure it properly, then buy with discipline.

If you're weighing an investment property refinance and want help deciding whether the move improves your position, speak with the team at We Are Buyers Agents. They work with investors and buyers across Australia from Sydney and Byron Bay, and can help you think through the refinance decision in the context of what you buy next, not just the loan you replace.