Two investors can start with the same deposit, buy in the same month, and still end up with completely different outcomes. One picks a suburb because it feels familiar, the other picks a location because the numbers and the local story line up. Five years later, the first investor owns a property that's been hard to lease and expensive to hold. The second owns an asset with stronger rent, better tenant demand, and a clearer path to long-term growth.

That gap usually comes down to location selection.

In practice, the best investment property locations are not just the suburbs with the loudest headlines. They're the places where yield, vacancy, affordability, infrastructure, and buyer demand all support each other. In Australia, that often means weighing metro stability against regional income, and deciding whether you're chasing growth, cash flow, or a workable balance of both.

That decision also depends on your broader strategy. If you're comparing a straight investment purchase with a future lifestyle plan, this guide on investment property vs second home is worth reviewing before you shortlist locations. And if your goals extend beyond buy-and-hold into subdivision or construction, your location filter changes again because access to finance for property development affects what sites are viable.

Most clients don't need more suburb lists. They need a framework that stops them buying in the wrong market for the right-sounding reasons.

Table of Contents

- The Two Investor Paths Introduction

- Decoding the Data Key Metrics for Property Investors

- Beyond the Numbers Unlocking Future Capital Growth

- Australian Market Showdown Metro vs Regional Hotspots

- Suburb Spotlights Where to Invest in 2026

- Navigating Risks and Finding Reliable Data

- Your Next Step Partnering with a Buyers Agent

The Two Investor Paths Introduction

Property investors usually fall into two camps.

The first group buys where they already know the streets, the cafes, and the school catchments. That can feel safe, but familiarity often hides weak fundamentals. A suburb can be pleasant to live in and still be mediocre as an investment.

The second group treats location scouting like an evidence-based exercise. They look at rent relative to price, vacancy pressure, infrastructure, employment drivers, and whether the suburb's current reputation is ahead of or behind its actual fundamentals. That's the group that tends to avoid expensive mistakes.

What usually separates strong locations from weak ones

A good investment area doesn't need to be perfect. It needs to make sense.

Some markets produce solid rent but little upside in value. Others deliver long-term growth but strain cash flow from day one. The best investment property locations sit closer to the middle. They don't force you to choose a completely lopsided outcome unless that matches your strategy.

Three filters matter early:

- Income strength: Can the property hold itself reasonably well through the cycle?

- Demand depth: Are tenants and owner-occupiers both active in the area?

- Future drivers: Is there a credible reason this location should be more desirable in a few years than it is today?

Practical rule: If a suburb only works on one metric, it usually doesn't work well enough.

What clients often get wrong

The most common mistake isn't choosing a bad city. It's choosing the wrong micro-market inside a decent city.

I've seen investors focus so heavily on broad labels like Sydney, Brisbane, or Byron Bay that they miss the block-by-block differences that shape performance. One pocket gets tenant demand from hospitals, transport, and schools. Another nearby pocket carries flood risk, oversupply, or a weak resale pool.

That is why location scouting has to move past broad opinion. A useful process tests the data first, then pressure-tests the local story behind it.

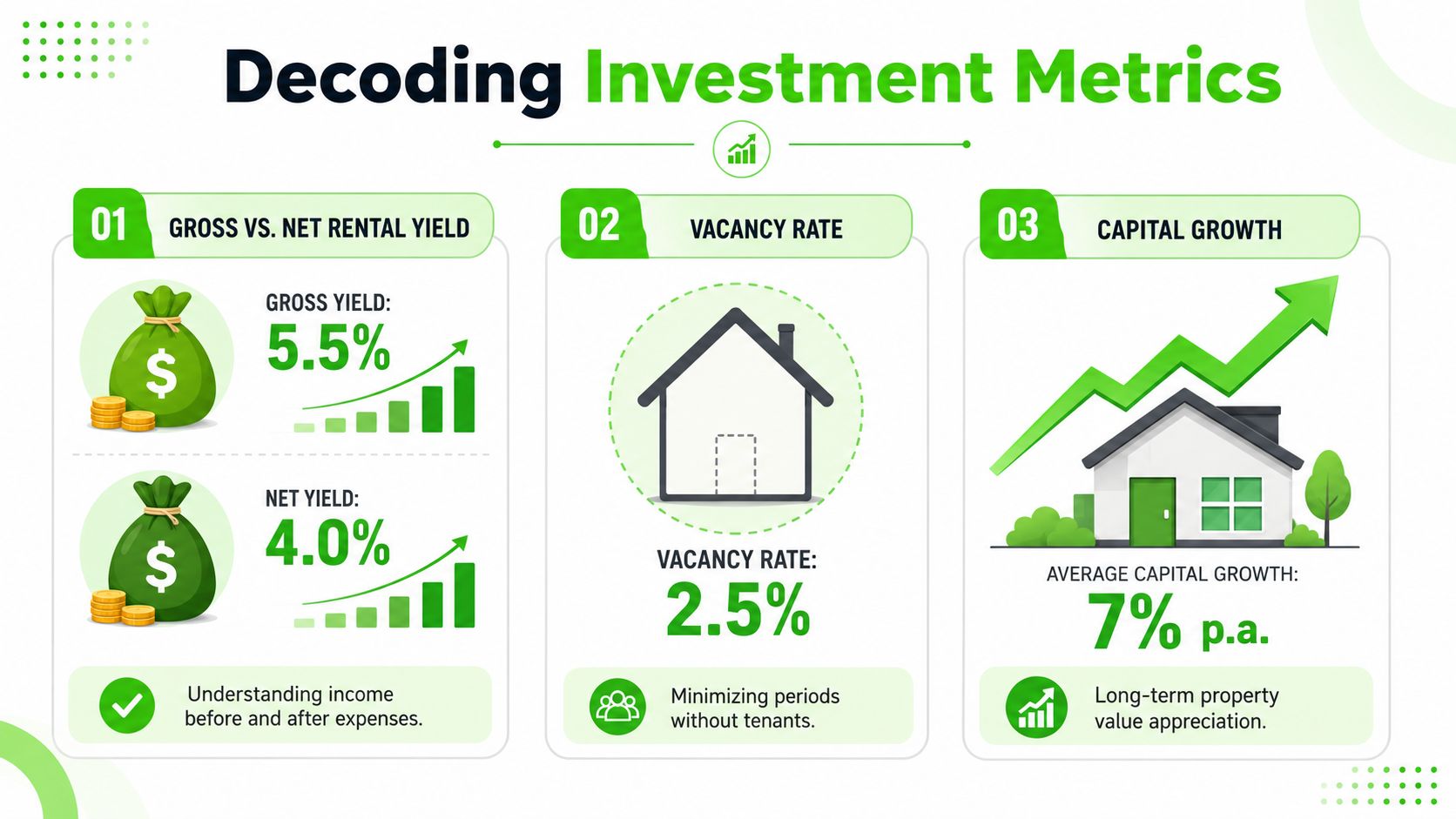

Decoding the Data Key Metrics for Property Investors

Investors often look at one number and decide too quickly. Yield looks attractive, so they assume the suburb is a winner. Or a market has a growth reputation, so they ignore the cost of holding it. Good decisions need a wider read than that.

Recent market commentary points to a real split in Australia. Regional NSW and Queensland are leading on rental yield in some areas with gross yields over 6%, while Sydney's average sits around 3.2%, according to reporting cited around CoreLogic trends in the Sydney Morning Herald. The same report included this line: "The post-pandemic sea-change and search for affordability has permanently rewired Australia's property investment map."

Yield tells you income, not quality

Gross rental yield is the rent collected relative to the purchase price, before costs. It's useful as a quick screening metric because it helps you compare suburbs without getting lost in detail.

But gross yield isn't your spendable return. Rates, insurance, management fees, maintenance, and vacancy all sit between gross rent and real cash flow. That's why investors also need to think in practical net terms, even when the initial suburb search starts with gross figures.

A high-yield suburb can still disappoint if tenant turnover is constant or if the local stock needs heavy ongoing maintenance.

Vacancy tells you bargaining power

Vacancy is where many spreadsheets become real.

A low vacancy setting usually means tenants don't have many alternatives. Landlords have more pricing power, leasing periods tend to shorten, and the risk of long empty stretches drops. A higher vacancy setting often points to oversupply, weak demand, or stock that isn't matching what renters want.

If you're comparing locations, pair yield with the suburb's rental conditions rather than treating them separately. For a practical way to assess that, a detailed rental market analysis helps connect advertised rent, stock levels, and demand patterns.

Capital growth matters, but context matters more

Growth is the metric many investors chase because it's what builds wealth over time. But historical growth on its own can mislead you.

Some suburbs rise sharply because they started from a lower base and were repriced by incoming demand. Others rise because infrastructure, jobs, and owner-occupier appeal keep reinforcing each other. Those are very different stories.

Strong investing isn't about finding the single highest yield or the suburb with the strongest recent growth. It's about understanding what produced those numbers and whether those drivers can persist.

A practical reading order

When assessing a location, I prefer this sequence:

- Start with yield to see whether the suburb has any income support.

- Check vacancy to judge how easy that rent may be to sustain.

- Review price point to understand entry risk and competition.

- Assess growth drivers to decide whether today's figures have tomorrow's support.

That order stops investors from falling in love with a suburb before checking whether it performs.

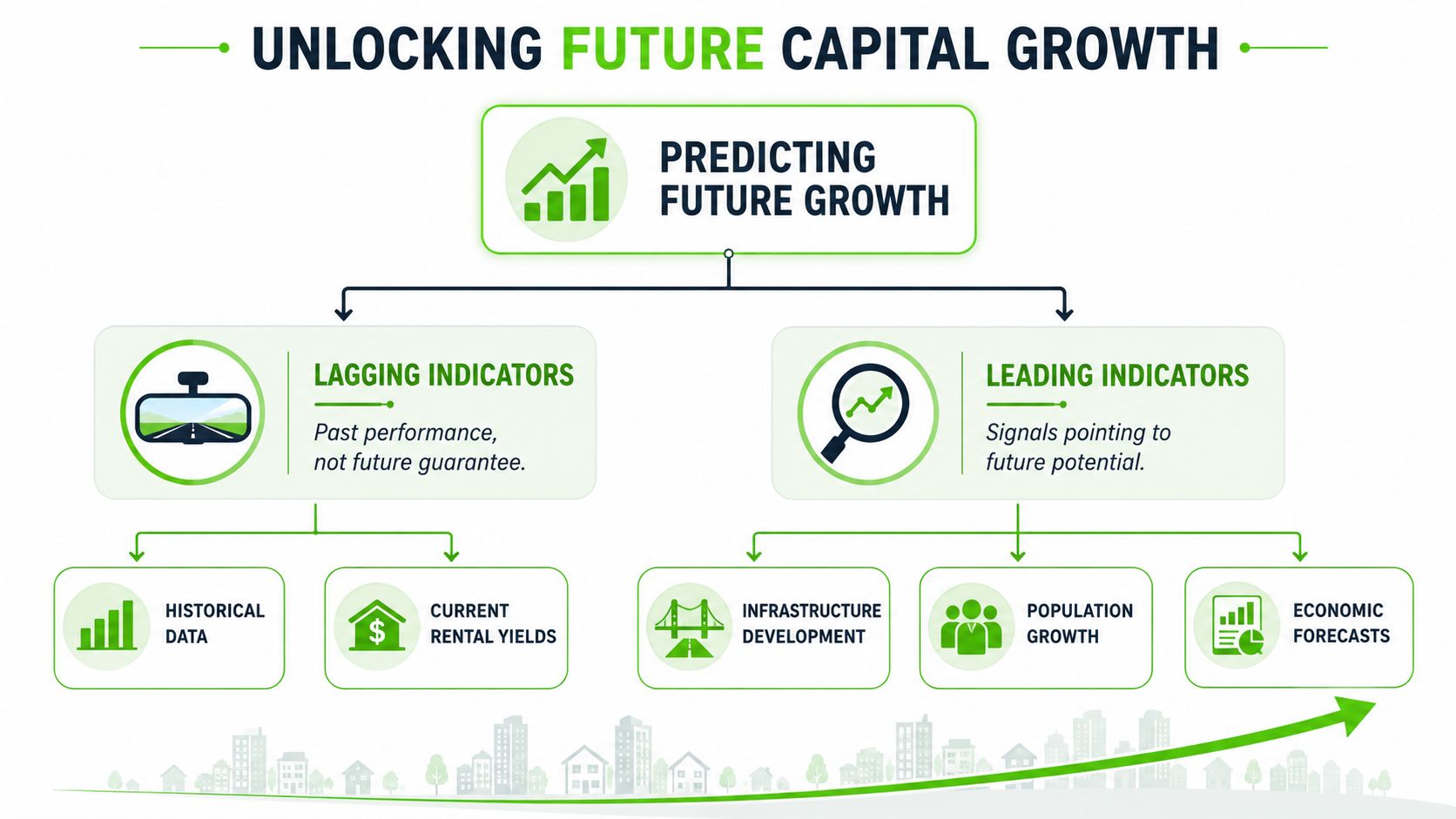

Beyond the Numbers Unlocking Future Capital Growth

The strongest investors don't just read current metrics. They ask what a suburb is likely to look like after the next wave of infrastructure, migration, and employer movement takes hold.

That's where many headline suburb lists fall short. They rank what's already visible. They don't always explain why one market is still early and another has already been repriced.

Infrastructure changes how people use a location

Transport links, hospitals, university expansion, and major retail or civic upgrades matter because they change day-to-day convenience. They also broaden the buyer and tenant pool.

When a suburb becomes easier to commute from, or when essential services improve, demand doesn't just increase in theory. More people are willing to live there, and more buyers can justify paying a premium to do so.

A useful overseas example shows the mechanism clearly. Dallas-Fort Worth has cash-on-cash returns exceeding 8.3% because median home prices allow for substantial financing, while strong job growth, including 30.5% corporate expansion, drives rental demand. The same market has shown annual appreciation of 10% to 12% due to infrastructure investment, as outlined by Forbes Advisor's real estate market review.

The exact numbers are U.S.-specific. The logic is universal.

Economic diversity reduces fragility

One-employer towns can perform well for a period, but they carry concentration risk. If that employer cuts back, the local property market can soften quickly.

Better long-term markets usually have several demand sources working at once. Health, education, logistics, professional services, tourism, and government employment don't all move in lockstep. That matters because diversified economies tend to absorb shocks better than narrowly based ones.

When I assess a suburb, I want to know whether local demand depends on one project, one mining cycle, or one dominant institution. If the answer is yes, the upside may still be there, but the risk profile is different.

Demographic shifts often appear before price moves

Population growth isn't enough on its own. You need to know who is moving in and why.

A suburb attracting young families usually behaves differently from one drawing downsizers or transient short-term tenants. Household type affects demand for dwelling style, renovation potential, school access, and lease stability. In Australian markets, these shifts often show up before they become obvious in median price data.

On-the-ground test: If new infrastructure is arriving, but the local housing stock doesn't suit the people likely to move in, growth can stall.

The best investment property locations usually show both. The hard data gives you confidence. The local qualitative drivers explain why that confidence might still be justified before the broader market catches up.

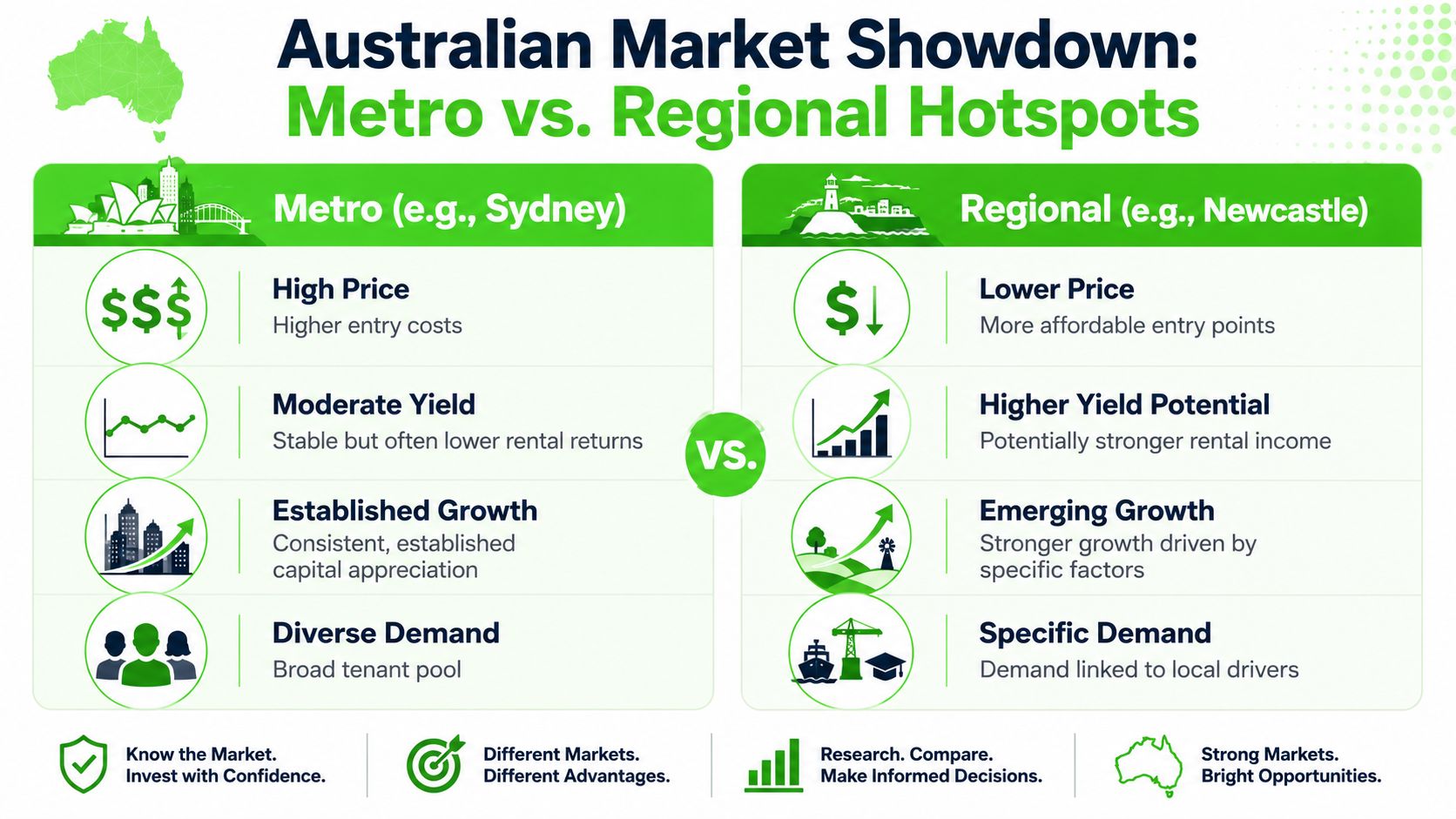

Australian Market Showdown Metro vs Regional Hotspots

The metro versus regional decision isn't really a debate about which is better. It's a question of fit.

Some investors need resilient demand and broad resale appeal, even if the yield is tighter. Others are willing to accept more operational complexity in exchange for stronger income or a lower entry point. That's why Sydney and lifestyle-regional markets such as Byron Bay or Northern NSW shouldn't be judged on the same standard alone.

Sydney and other major metros

Metro markets usually offer scale. There's deeper employment, a broader tenant base, more infrastructure, and a larger owner-occupier market that can support values over the long run.

That doesn't mean metro automatically wins. In many Australian capital city suburbs, the trade-off is obvious. Entry prices are higher, rental yield can be thinner, and holding costs are less forgiving if rates or vacancy move against you. Sydney, in particular, often suits investors who can tolerate lower income in return for stronger long-term scarcity dynamics.

Metro also rewards careful asset selection. In a strong city, the wrong apartment in an overbuilt precinct can underperform even while nearby houses or boutique blocks do well.

Regional and lifestyle markets

Regional markets can produce a more attractive income profile, especially where affordability and tenant demand line up. They can also benefit from migration shifts, lifestyle appeal, and reduced competition from owner-occupiers compared with blue-chip metro areas.

But regional investing isn't passive. Local economies can be narrower. Sales volumes can be thinner. Certain lifestyle markets also face tighter planning controls or changing attitudes toward short-term accommodation.

AirDNA's projected analysis for 2026 argues that many best investment property locations lists overemphasise headline cities and ignore vacation-rental micro-markets, while smaller locations can show strong short-term rental yield and cash-flow potential. The key question, according to AirDNA's vacation rental investment analysis, is which neighbourhood has enough demand, regulation certainty, and occupancy to outperform.

The real trade-off

A Sydney asset may appeal to an investor who wants deep demand and a more liquid resale market. A Byron Bay or Northern NSW asset may appeal to someone comfortable with sharper market cycles, stronger lifestyle-led demand, and greater management sensitivity.

Here is the practical divide:

- Metro suits investors who value depth: broader tenant demand, more diverse employment, and stronger resale liquidity.

- Regional suits investors who value income or thematic growth: affordability, migration trends, and targeted local catalysts.

- Lifestyle markets suit investors with hands-on risk tolerance: these markets can be compelling, but regulation and management quality matter much more.

If a regional market only works while everything goes right, it's not a strong market. It's a fragile one.

Suburb Spotlights Where to Invest in 2026

A shortlist should never be built from one national ranking. It should come from matching your budget and risk tolerance to the kind of demand a suburb can realistically sustain.

The examples below aren't presented as universal picks. They show how to think. In practice, investors should build a suburb case around affordability, rentability, transport access, employment anchors, and whether the local buyer pool is expanding.

Western Sydney growth corridors

In Western Sydney, I look for suburbs where infrastructure is reshaping commute patterns and where owner-occupiers are gradually lifting the quality of the housing stock. These areas can work well when tenants want access to jobs, schools, and transport but can't stretch to more established inner and middle-ring locations.

The mistake here is buying purely on affordability. Cheap stock near transport noise, flood exposure, or heavy investor concentration can underperform even within a growth corridor. The better opportunities are usually in pockets where family demand is broadening and resale isn't limited to investors alone.

South East Queensland regional cities

Regional Queensland keeps attracting investor attention because it often offers stronger income settings than the large southern capitals. But suburb choice matters more than state-level enthusiasm.

In these markets, I prefer established residential pockets close to hospitals, education, and daily retail rather than fringe estates that depend on future demand showing up exactly as planned. When local employment is diversified and the suburb has practical liveability, rent demand is often more durable.

A useful way to frame this balance comes from the U.S. example of Indianapolis, where a 9.1% gross rental yield, a median home price of $268,000, and 38% five-year price appreciation showed how affordability and strong rental demand can work together, as outlined in AmeriSave's investment market guide. The takeaway for Australia isn't that we copy Indianapolis. It's that balanced markets usually outperform "story-only" markets.

Perth cash flow pockets

Perth often comes up when investors want a better income profile, but not every suburb offers the same risk-adjusted value. Some locations look strong on headline rent and then fall apart on tenant profile, stock quality, or resale depth.

For investors specifically exploring stronger holding income in WA, this breakdown of Perth's best cash flow suburbs is a practical starting point because it narrows the search to areas where rent performance is part of the thesis, not an afterthought.

Before adding any Perth suburb to a buy list, I still want to see whether demand comes from stable local drivers or from a narrow market segment that could cool quickly.

Lifestyle-driven markets in Northern NSW

Lifestyle markets can tempt investors because demand is visible. The town feels busy, holiday traffic is obvious, and the local brand is strong. That's not the same as saying every property there is a good investment.

In Northern NSW, especially around coastal and lifestyle areas, the right asset can benefit from limited supply and strong desirability. The wrong asset can be exposed to planning limits, seasonal fluctuations, insurance pressure, or overly optimistic assumptions about rent.

This video gives a useful overview of what investors should watch in the current market before narrowing a shortlist.

2026 Investment Suburb Snapshot

| Suburb Example | Median Price | Gross Yield | Vacancy Rate | Key Growth Driver |

|---|---|---|---|---|

| Western Sydney growth corridor | Varies by pocket | Typically lower than many regional markets | Must be checked suburb by suburb | Transport and employment infrastructure |

| Regional Queensland city suburb | Varies by city and stock type | Often stronger than Sydney-style metro markets | Must be checked locally | Affordability and diversified services employment |

| Perth cash flow suburb | Varies across metro and outer-metro areas | Can suit income-focused investors | Must be checked at suburb level | Relative affordability and rental demand |

| Northern NSW lifestyle pocket | Varies widely | Depends heavily on long-term vs short-term strategy | Sensitive to regulation and seasonality | Lifestyle demand and constrained supply |

Good suburb selection sounds less exciting than hotspot marketing. It also tends to produce better results.

Navigating Risks and Finding Reliable Data

A promising location can still become a poor investment if the risk work is sloppy.

I see this most often when buyers rely on one portal, one sales agent's opinion, or one suburb report without checking the details that affect holding costs and exit risk. Flood overlays, bushfire constraints, zoning changes, body corporate issues, and nearby unit supply can all damage performance even in a market with strong broader demand.

Risks that deserve real attention

Some risks are obvious. Others are easy to miss until you've already exchanged.

- Planning risk: Council rules can affect development potential, renovation scope, and short-term rental use.

- Oversupply risk: New apartment or townhouse pipelines can dilute rent growth and resale competition.

- Environmental risk: Flood, bushfire, coastal exposure, and insurance limitations need property-level review.

- Interest rate sensitivity: A suburb that only works with perfect borrowing conditions is already on shaky ground.

Where to verify your assumptions

Use multiple sources and compare them rather than looking for one platform to do everything.

CoreLogic is useful for sales history and broad suburb performance. SQM Research helps investors track vacancy and asking rent trends. State planning portals and council mapping tools are essential for zoning, flood, and overlay checks. The Australian Bureau of Statistics helps with population, household, and workforce context.

A practical workflow looks like this:

- Screen the suburb using market data platforms.

- Check planning overlays through council and state tools.

- Review local supply by looking at development applications and current listings.

- Pressure-test tenant demand with property manager feedback from the exact pocket you're targeting.

This is also where service providers can help. A buyer may use CoreLogic and council tools directly, or engage a specialist such as We Are Buyers Agents to narrow locations and assess micro-market risk before purchase.

What reliable due diligence feels like

Reliable research usually makes a suburb look less perfect. That's a good sign.

If every source says the same glowing thing and none of them mention trade-offs, you probably haven't gone deep enough. The aim isn't to find a suburb with no risk. It's to find one where the risk is visible, manageable, and matched to your goals.

Your Next Step Partnering with a Buyers Agent

Finding the best investment property locations takes more than scrolling suburb rankings on a weekend. The hard part isn't generating a list of possibilities. It's removing the suburbs that look fine on paper but fail when you examine supply, tenant depth, flood exposure, resale appeal, and street-level differences.

That's where a buyer's agent can earn their place in the process.

A good advisor doesn't just say which city is popular. They compare micro-markets, filter stock that doesn't suit your strategy, and negotiate with a clear view of what the property should deliver. For investors buying outside their home market, that local reading becomes even more important because broad suburb data rarely captures the difference between one strong pocket and one risky pocket a few streets away.

If you're weighing metro versus regional, balancing yield against capital growth, or deciding whether a lifestyle market is really investable, it helps to work with someone who does this every day. This overview of a buyer's agent in Australia explains how that support typically works across search, due diligence, and negotiation.

The best results usually come from a disciplined process. Define the brief clearly. Filter locations hard. Verify the local story. Then buy the right asset in the right pocket at the right price.

If you'd like help narrowing the best investment property locations for your budget and strategy, book a consultation with We Are Buyers Agents.